Weekly Economic Digest for 10-13-23: Oil; Producer and Consumer Prices; Consumer Sentiment; and Krugman Strikes Again

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Last week we all thought that the ousting of the Speaker of the House for the first time in history was big news. Little did we know that just a few days later, a new war in the Middle East would push that story right to the back burner! There wasn't very much economic data released this week...just numbers on consumer prices (CPI) and producer prices (PPI). But both of those will be affected in the near future by the price of oil which is certain to be impacted by the Israeli-Palestinian conflict.

Oil

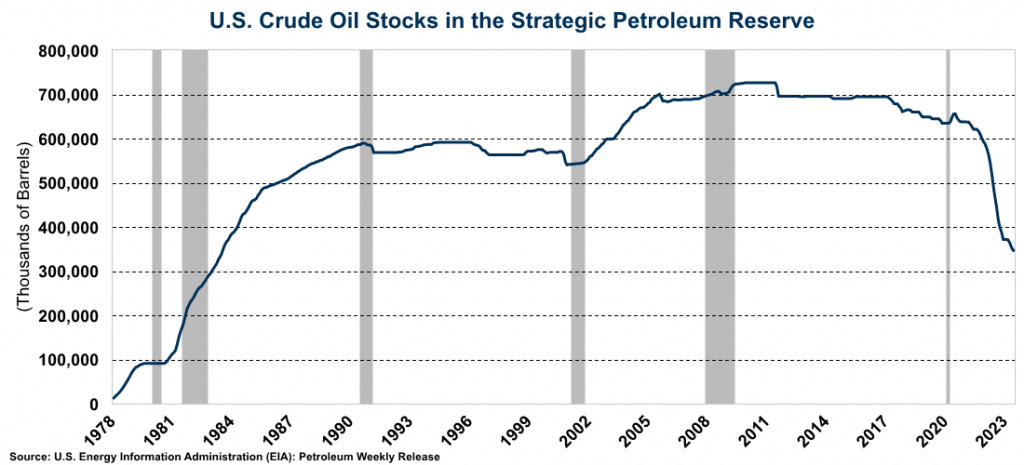

Speaking of oil, even before the events of last weekend, the price of oil was headed up and was likely to break the $100/barrel price point. Luckily for us, as a hedge against global instability in the oil market, we have our Strategic Petroleum Reserve (SPR) which, according to the U.S. Department of Energy, is "the world's largest supply of emergency crude oil" and "was established primarily to reduce the impact of disruptions in supplies of petroleum products."

Good thinking. Glad we have that going for us...oh wait.....

In January 2021, we had 631 million barrels of oil in the SPR. In the U.S. we use roughly 19 million barrels per day, meaning that we had a little more than a month's worth of oil in the SPR to help smooth out supply disruptions. Unfortunately, since 2021 we haven't used it to smooth out supply disruptions. Instead, we used it to offset the pain of inflation brought about by irresponsible fiscal policy. Since 2021, the current administration has depleted nearly HALF of the SPR to help offset the rising price of gas in support of their own political objectives. That is NOT what the SPR was designed for, nor how it should be used. We now have about 18 days of oil in the SPR, and we are at the lowest level we have seen since July 1983. We had $100+ oil for most of 2011 through 2014, yet we kept the level in the SPR constant. Why? Because that oil was to be used for STRATEGIC purposes...not POLITICAL purposes. If the war in the Middle East evolves into a larger regional conflict, we could find ourselves in a very precarious position with respect to our oil supply.

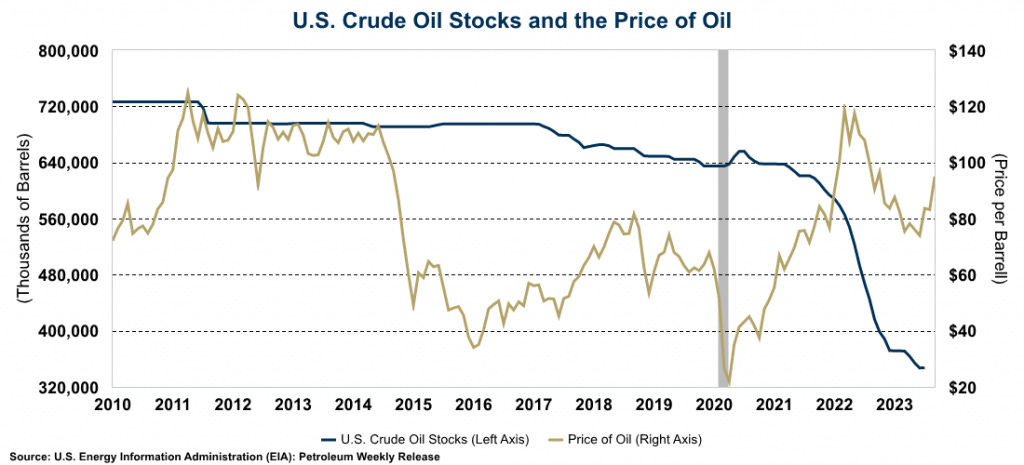

There is one bright spot however, and this may be a surprise given what the media has been reporting. Despite a significant decline in the number of active rotary rigs, U.S. crude oil production has exploded since July and is now at 13.2 million barrels per day...higher than the previous peak in 2019. This has helped to offset the drop in OPEC production, and, while it won't meet all our daily needs, it is a step in the right direction.

Producer Price Index

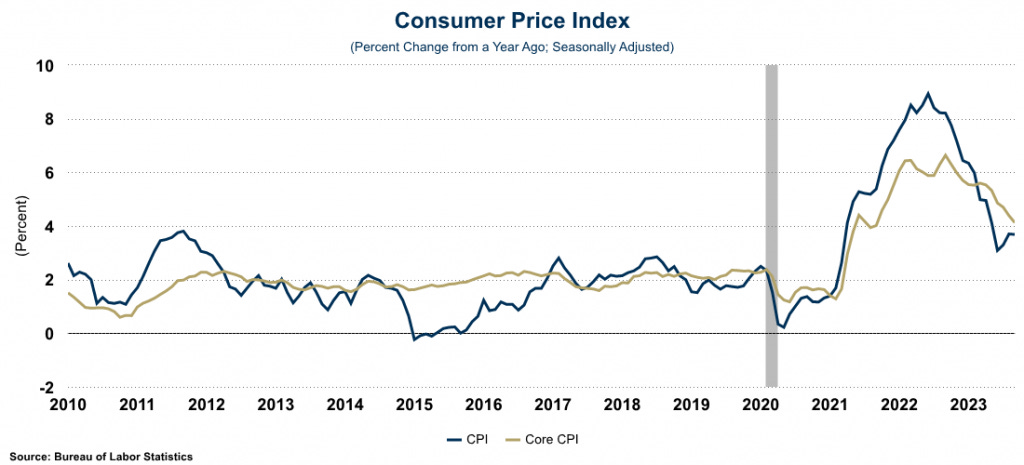

On Wednesday, the government released September data on producer prices. Producer prices jumped 0.5% month-over-month, much faster than the 0.3% that economists were expecting. Year-over-year, prices at the producer level are running 2.2%. However, goods inflation jumped to 2.5% (the third consecutive increase) due in large part to the increase in energy prices. Core goods are up 2% year-over-year. However, service inflation continues to be high running 2.8% in September. As can be seen in the graph below, producer prices seem to have halted their downward trend and are now flat to increasing, which could lead to higher prices at the consumer level.

Consumer Price Index

Speaking of the consumer level, on Thursday, the government released September data on consumer prices. "Experts" were expecting CPI to pull back in September. However, the inflation rate remained steady at 3.7%. Core CPI, (CPI less food and energy) is still running over 4% on an annual basis. Shelter costs were the largest contributor to the gain, accounting for over half the increase. Shelter inflation is running at more than 7% and has been running that hot for more than a year. As pointed out two weeks ago, housing prices continue to rise, despite very high mortgage rates due to limited supply.

As we pointed out last month, inflation running at 3.7% doesn't sound too bad, but prices are significantly higher than they were in 2021. When we say "prices are 3.7% above September 2022" we need to remember that in September 2022, they were 8.2% above September 2021! And, in September 2021, they were 5.4% above September 2020! Overall, prices are 17.1% higher than they were in January 2021. Food is 19.6% more expensive now than it was in January 2021, and energy is a whopping 38.8% more expensive that it was in January 2021. Auto insurance is running 35.6% higher than it was in January 2021. Housing, food, energy, auto insurance...these are not discretionary items. These are costs that most households are required to deal with every day and they are still increasing at a rapid rate.

And, according to the University of Michigan Consumer Sentiment Survey (released today), consumers are expecting higher prices over the next 12 months as their inflation expectations rose to 3.8% this month.

Overall, consumers sentiment plunged to 63.0 lead by a big drop in consumer expectations about the future of the economy.

Wages

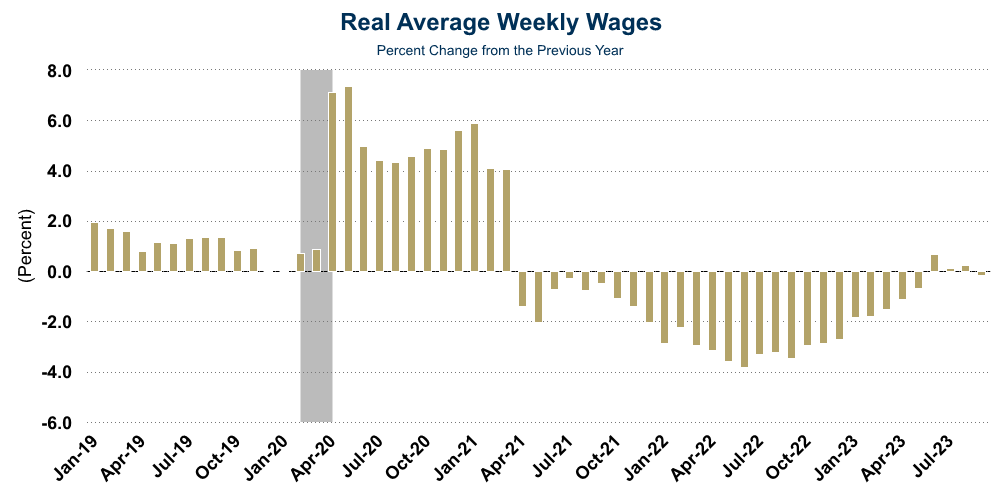

And why wouldn't consumers be less optimistic about the future? While inflation continues to climb, wages are not keeping up. After 26 months of decline, real wages (i.e., wages adjusted for inflation) posted three consecutive months of small increases. However, in September, real wages fell once again.

To make ends meet, people continue to increase their credit-card borrowing. For the 18th consecutive month, revolving credit borrowing grew at double-digit rates. Next week we will get information on retail sales, and it will be interesting to see just how strong the consumer really is. My bet....they are starting to get get tapped out and the contribution to GDP of personal consumption in the 4th quarter will be significantly less than in recent quarters....despite current forecasts of a record holiday season. Frankly, I just don't see consumers going crazy this Christmas.

He Said What?

One final note this week. On September 15, we introduced a segment called "Stupid Economic Statement of the Week" and the initial recipient was Paul Krugman, Distinguished Professor of Economics at the Graduate Center of the City University of New York. We are back with the second installment, and it turns out that Paul Krugman is the gift that keeps on giving. Below is a tweet he put out yesterday...

So, Krugman tells us that "the war on inflation is over." And to support this assertion, he uses CPI, but he takes out food, energy, shelter, and used cars. Right. Because, who among us needs food, energy, shelter, or a car? Granted, it has probably been a while since Paul Krugman bought a used car, (people with Nobel Prizes do not shop for used cars) but for the rest of us, food, energy, shelter, and used car prices are important and take a large share of our household budgets.

As we pointed out on 9/15, Milton Friedman famously said, "inflation is always and everywhere a monetary phenomenon." The inflation of mid-2022 was due to the rapid increase in the money supply in mid-2020. There is a lag of at least 12-18 months before changes in the money supply work their way through to prices.

So, the brief disinflation (or temporary slowing in the pace of price increases) we have seen recently is a result of the attempt by the Fed to decrease the money supply. But from the graph above, it is clear that the money supply is once again increasing. And that simply means that there is more inflation to come.

So no. The "war on inflation" has not been won. Not even close. The issue of course is that Krugman is trying to push his ideological position despite evidence to the contrary. It doesn't matter on which side of the political spectrum you find yourself...when you let your political ideology usurp your common sense, you simply end up looking foolish. So you keep tweeting Paul! We might have to add a weekly segment called "Krugman Tweets" if for no other reason than it gives those of us in the real world a good chuckle in an otherwise rough economy.