Weekly Economic Update 03-20-26: GDP 4th Quarter (revised); JOLTS; Home Builder Confidence; New Home Sales; and the Producer Price Index

The economy at the end of last year was significantly worse than originally reported.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

The State of Georgia Senate passed S.B. 424 this week, which recognizes gold and silver as legal tender in the state and establishes a state-approved bullion depository where people can open an account to hold physical gold as a hedge against inflation and the constant devaluation of the dollar by the Federal Government. Account holders would be able to access their gold via a debit card to make purchases everywhere from Publix to Costco to Chick-fil-A.

I don’t usually say this about legislation, but this is a FANTASTIC idea. Senator Marty Harbin, R-Tyrone, the sponsor of the bill, is to be commended.

Of course, there is the usual cadre of academics who are critical. For example, in this particular article, Campbell Harvey, a finance professor at Duke University, doesn’t like the idea and says, “There is no guarantee that it will provide a hedge for inflation in the short term.” I have seen similar comments on social media from economics professors within Georgia’s own university system.

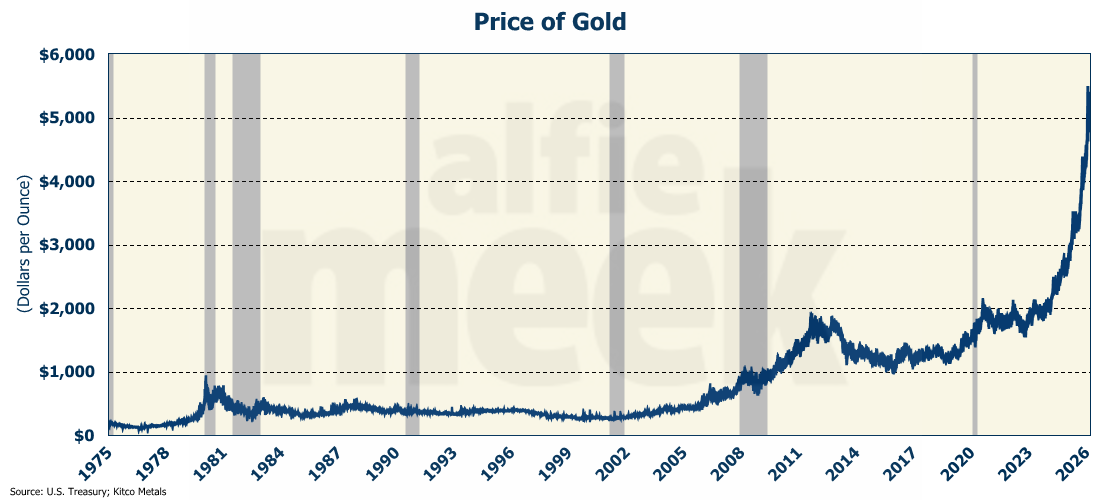

As usual, Mr. Harvey and those of his ilk completely miss the point. This isn’t intended to be a short-term instrument. Mr. Harvey is correct that, in the short term, gold does fluctuate, sometimes quite significantly (as we learned this week). However, as I have often demonstrated, over the long term, gold is a hedge against inflation, a store of value, and protection against the grossly irresponsible fiscal policies of our federal government. I pointed out a few weeks ago that you could have bought the median-priced new home in 1980 for 93 ounces of gold. You could still purchase the median-priced home in 2025 for 93 ounces of gold. Gold isn’t an investment. It is money. Real money.

People have asked me how this system would work. It is really quite simple. In fact, I personally have been doing this for several years via a private company called Glint. (This is not meant in any way to be an endorsement of Glint, but rather a real-life example of the Senate proposal.) I have an account with Glint where they hold physical gold in my name in a Brinks vault in Switzerland. I have a debit card that I can use anywhere that accepts debit card payments to pay for goods and services with that gold. When I make a purchase, the vendor gets cash, and that amount of gold is removed from my account at the current dollar price of gold. Similarly, I can send cash to Glint, and they will add gold to my account at the current dollar price.

One of the criticisms of holding physical gold is that it isn’t very liquid. I personally have never had a problem turning physical gold into cash, but I understand the point. Gold should be a long-term hedge against inflation, but when you need it, you need it. Having a debit card linked to your gold solves that problem.

Keep reading with a 7-day free trial

Subscribe to Alfie Meek's Weekly Economic Digest and Commentary to keep reading this post and get 7 days of free access to the full post archives.