Weekly Economic Update 04-04-25: Liberation Day; ISM Manufacturing; Factory Orders; ISM Services; JOLTS; and March Employment

Conflicting hard and soft data on the manufacturing sector, as well as overall employment, raise questions about the true strength of the economy.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Liberation Day finally arrived! I’m not all that clear about what we are being liberated from, but I think it is supposed to be from unfair trade barriers from other countries. I didn’t feel particularly oppressed by those other countries, but perhaps I had fallen victim to some form of Stockholm Syndrome.

However, it does appear that I was liberated from a significant portion of my retirement portfolio. But retirement was probably just a pipe dream anyway.

Just over 100 years ago, David Ricardo developed the classical theory of competitive advantage, which taught us that if two countries focus on those things in which they have a comparative advantage, and then engage in free trade, both countries will be better off.

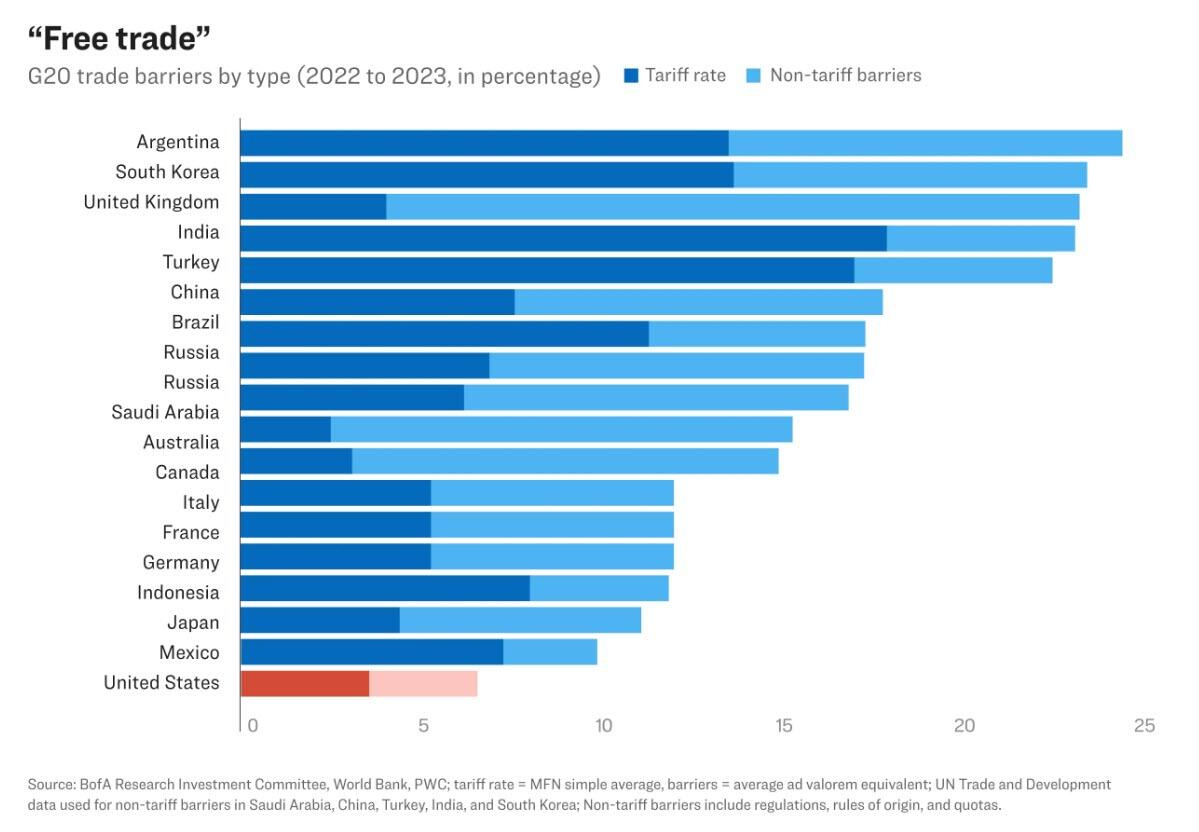

But this only works when everyone plays by the same rules. And not everyone is playing by the same rules. Other countries have lower labor standards, lower environmental standards, and higher levels of government intervention. According to Bank of America, the United States has the lowest trade barriers of any G20 nation. (G20 is a group of 20 nations that represent the world’s largest economies.).

That doesn’t seem “fair” (whatever that word means), and it certainly doesn’t conform to a Ricardian view of international trade. In a world where trade is distorted by these differences, tariffs don’t necessarily introduce inefficiency. In fact, they can actually work to counteract it and move you toward a more efficient outcome.

The president rolled out a series of mostly reciprocal tariffs. The word “reciprocal” is very important here. According to the Merriam-Webster Dictionary, the definition of “reciprocal” is:

inversely related

shared, felt, or shown by both sides

consisting of or functioning as a return in kind

These tariffs were mostly in response to tariffs and other non-tariff trade barriers that other countries were already imposing on us.

The German philosopher Friedrich Nietzsche wrote, “That which does not kill us makes us stronger.” IF the administration sticks with these proposed tariffs (and that is highly unlikely as nations come to the table to negotiate), once all the dust settles, the U.S. should find itself in a much stronger economic position and one with more equitable international trade arrangements. However, the journey from here to there may come with some level of discomfort. Short-term pain for long-term gain. But, as British economist John Maynard Keynes (and more recently Sen. Kennedy) pointed out, "In the long run we are all dead."

Obviously, we are all better off if we can get to reciprocal tariffs of zero! I believe the administration expects this is where these tariffs will eventually take us - to a more level global playing field. I just hope getting there doesn’t kill us first.

ISM Manufacturing

Despite the fact that the “hard data” continues to impress, the “soft data” for the manufacturing sector continues to weaken. For example, factory orders were up (see below) but the ISM Manufacturing survey in March fell from 50.3 to 49.0 (lower than the 49.5 that was expected and below the critical 50 level), which is the lowest reading since the November election (full release here).

Looking deeper at the survey components, the picture gets a little more troublesome. The index for new orders has fallen for the past two months, as has the index for employment, and both are well below 50. (This is odd because according to ADP data released this week, the US economy added 21k manufacturing jobs in March, the most since October 2022 and more than the 120k expected and almost double the 77k added in February.)

But even more concerning is the index for prices paid by manufacturers. It has now risen for four consecutive months and is increasing at an accelerating pace. It is now at 69.4 which is the highest it has been since June of 2022 when the CPI peaked at 9%!

As I have said many times over the past two years, inflation is not beaten and is, in fact, coming back. The question I have regarding this survey is this…is this actual inflation that manufacturers are experiencing, or is it anticipatory of coming tariffs? It is supposed to be the former, but I fear that it may contain a bit of the latter.

Factory Orders

However, unlike the “soft data” above, the hard data shows that manufacturing continues to recover. For the second month in a row, factory orders for U.S. manufacturers rose - both with and without transportation (full release here). Overall, factory orders were up 0.6% in February, which was higher than expected. Year-over-year orders were up 2.5%. “Core” orders (orders less transportation) were up for the sixth consecutive month and rose 0.4% in February. Year-over-year, they are up 1.8%.

There is simply no indication of a slowdown in manufacturing in the first quarter, and despite what the Atlanta Fed is saying, I don’t see any evidence to support negative GDP growth for the first three months of this year.

ISM Services

So, the manufacturing sector may or may not be recovering, based on which data you prefer. Apparently, the service sector is taking a hit as well. The ISM Services index for March fell to 50.8 - its lowest level since June 2024, when it dipped briefly below 50 (full release here).

Any reading above 50 means the sector is expanding, but the drop is concerning. Employment in the service sector dropped sharply into contraction territory, and new orders fell off as well. The only possible good news from the March numbers is that prices paid in the service sector fell slightly.

As with manufacturing, the “soft” data certainly portends a slowdown. The question is, will the hard employment data back that up? If so, the threat of stagflation remains with slowing economic growth and rising inflation.

Job Openings, Layoffs, and Turnover Survey (JOLTS)

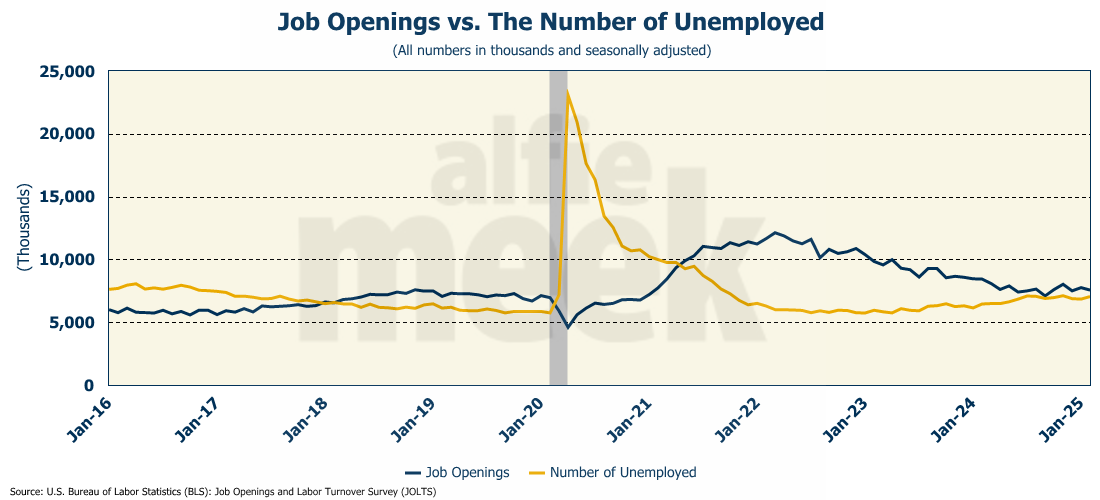

The number of job openings fell in February to 7.568 million, a drop of nearly 200K from January and down more than 875K from a year ago (full release here).

There were significant declines in job openings in finance and insurance (-80K); trade/transportation/utilities (-163K); private education/health (-33K); and leisure and hospitality (-61K). On the flip side, there was an increase of 134K job openings in professional/business services.

Job postings on Indeed.com fell 10% year-over-year last week to the lowest in 4 years. Over the last 3 years, job postings have dropped 33%, and NEW job postings have fallen 40% since February 2022.

Even so, the number of job openings still exceeds the number of unemployed. A recession has never started when there were more job openings than unemployed workers. However, it does appear that we are getting close to an inversion.

March Employment

This leads us to the latest read on the overall labor market. Once again, the hard data is performing much better than the soft data. The U.S. economy added 228K jobs in March, far more than the 140K that were expected (full release here).

Per usual, healthcare added a lot of jobs, and so did retail as the consumer continues to spend. But the overall positive news is that job growth was primarily in the private sector, which added 209K jobs. For many years, most of the job growth has been in government. In March, federal government employment declined by 4K. (Most of the DOGE cuts happened after the survey week.)

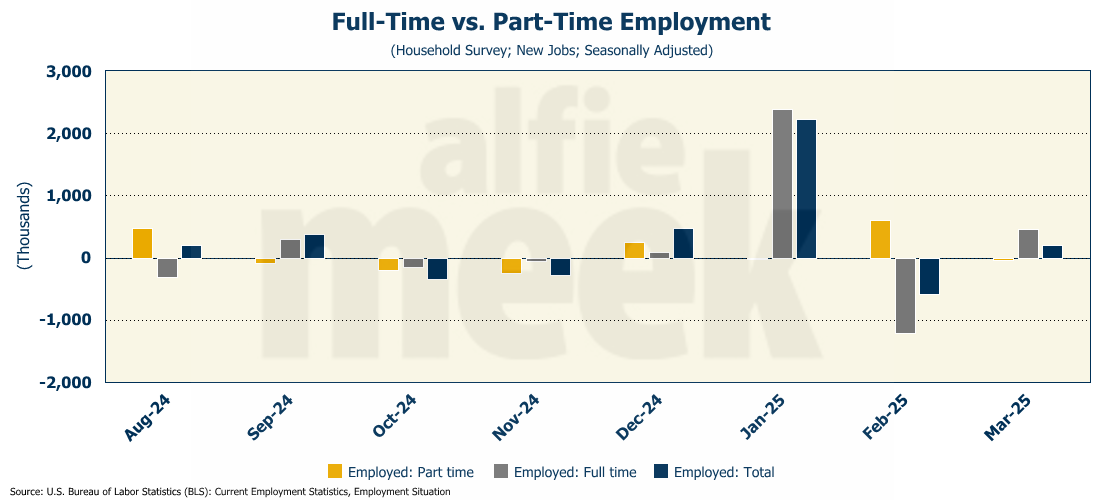

The household survey also showed an increase of 201K jobs. For once, the growth was in full-time jobs which were up while part-time jobs actually fell. That is not the pattern we have seen in recent months, and it is a welcome change of pace.

The unemployment rate ticked up slightly to 4.2% as the labor force participation rate rose to 62.5%. On a year-over-year basis, wages were up 3.8%. However, adjusted for inflation, real hourly earnings were up only 1.2% while real weekly earnings were up 0.8%. Weekly earnings are lagging hourly earnings because the average work week continues to fall.

One More Thing…

In the first post of the month, I try to recognize my gold and silver members. Special thanks to my only “gold” level member, Andrew Hajduk, and my “silver” level members, Dan McRae, C. Fitch (I don’t have a full first name), and William Whitlock. These four are very generously supporting this update every month, and it is very much appreciated.

If you are a regular reader and find this useful, please consider a membership. I invite you to click/scan the QR code below to join or just “buy a coffee!”

Next week, I will be taking some personal time off, and I am considering, for the first time in nearly two years, not producing the update. We’ll see how it goes. If you don’t see an update on the 11th, it will certainly be back on the 18th.