Weekly Economic Update 05-17-24: CPI & PPI; Retail Sales; Home Builder Confidence; Housing Starts; Building Permits; Industrial Production; and Leading Economic Indicators

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

First this week, I want to thank the group at the LaGrange-Troup County Chamber breakfast where I spoke on Tuesday morning. It was a great group and they listened fast as I crammed a one hour presentation into about 25 minutes! But there were a lot of good questions afterwards and several of them are new subscribers to this weekly update!

I also want to thank the Business Executives for National Security (BENS) Southeast group for asking me to speak at their lunch meeting on Wednesday. The conversation Tuesday night at dinner was enlightening and I certainly hope that the members found something useful in my remarks.

There was a lot of data released this week, so let's get to it.

Producer Price Index

First out of the blocks this week was the Producer Price Index (PPI). For the fourth month in a row, the index came in much hotter than expected. Producer prices rose 0.5% in April, to a level 2.2% higher than last year. Core final demand (less food, energy, and trade services) is running 3.1% year-over-year. PPI for services is running at 2.7%. In fact, the PPI for services grew 0.6% in the month, the hottest read since July of last year and that increase was the driving factor moving the overall PPI up. The main driver of services is labor cost, and we saw two weeks ago that employment costs were up significantly in the first quarter.

Every day, it becomes more and more clear that the Fed does not have inflation under control. A simple look at the graph shows that prices across the board are once again rising at an increasing rate. In fact, for the first time in more than a year, NONE of the underlying factors in the PPI were negative. The cost of everything is rising. And producer prices tend to lead consumer prices. Speaking of which...

Consumer Price Index

Consumer prices came in slightly lower than expectations at 0.3%. Year-over-year, the rate fell to 3.4%. That sounds like a move in the right direction. However, 0.3% is still much hotter than the Fed would like. And, if you annualize the monthly growth, it is running at a 3.8% annual rate. In fact, if you take the growth for the first four months of the year, and annualize that, CPI is running at 4.6%! Put that way, it doesn't sound too good.

But what is most concerning is the core services less shelter index. Services represent 2/3 of consumer spending, and the CPI there is running 5.6% on an annualized basis over the first four months of the year. Digging a little deeper we see the following annual rates of service inflation: car insurance - 22.6%; transportation - 11.2%; hospital services - 7.7%; car repairs - 7.6%; electricity - 5.1%; and food away from home - 4.1%.

Overall, CPI is up 19.2% since January 2021. Food is up 21%; energy is up 37%; and auto insurance is up 52%. There is simply no argument to be made for the Fed to cut rates any time soon.

Retail Sales

Retail sales were absolutely flat in April as consumers pulled back spending on furniture, vehicles, and health care products. But the biggest decline was in on-line sales. Sales jumped at gas stations, as the price for a gallon of unleaded gas started the month at $3.47 and ended more than 4% higher at $3.62.

"Core" retail sales (which removes automobiles, gasoline, building materials, and food services as they are volatile and can skew the results) fell 0.3% in the month, after posting a huge jump in March. But this brings up a point I made last month...Easter was in March this year and that means that March should be unusually strong and a pullback in April was expected. I say "was expected"....I certainly expected it. Apparently, "economists polled by the Wall Street Journal" expected an increase of 0.4%. But, with March being so strong; consumer confidence falling off a cliff last week; and revolving debt posting zero growth, these weak numbers for April should surprise no one. Frankly, it is starting to look like the consumer may have finally hit a wall.

Home Builder Confidence

If consumer spending hasn't hit a wall, home builder confidence certainly has! With the 30-year mortgage rate back above 7, home builders are seeing home buying activity slow and their expectations are that sales will fall over the coming months. In fact, the index for the 6-month outlook fell 9 points! That is the largest monthly drop since late 2022. This month, 25% of builders say they are cutting prices to attract buyers (up from 22% in April). In addition, 59% say they are using some sort of incentives (other than price cuts) to move houses.

The only thing supporting builder confidence is the fact that they are the only ones adding supply to the market! Given that the 30-year mortgage rate is 320 basis points above the average rate on existing mortgages, few homeowners are willing to put their house on the market which is severely limiting supply and keeping prices sky high.

Housing Starts

I mentioned above in the retail sales paragraph about "experts" expectations. Every time a piece of economic data is released, the data is always compared to what "experts" thought would happen. I often wonder who these "experts" are and how they derive their expectations? They are usually listed as "analysts" or "Wall Street economists," etc., and I assume they have sophisticated models and computer programs that help them with their forecasts. But, as a great economic forecaster taught me in graduate school, we can become too dependent on our models and forget to use our common sense. For example, we have soaring mortgage rates, plunging consumer sentiment, and weak home builder sentiment and yet, for some reason, the "experts" expected a big jump in both housing starts and building permits.

Housing starts did rise 5.7%, but that was driven entirely by multi-family housing, and even then, only because they revised the data for March down significantly! In fact, the March number was revised so low, that the April "bounce" was coming off lows that equal those seen at the beginning of COVID! Even with the April bounce, multi-family starts are still trending down. Single-family starts were down for the second month in a row falling 0.4% and have been relatively flat since the fall of last year.

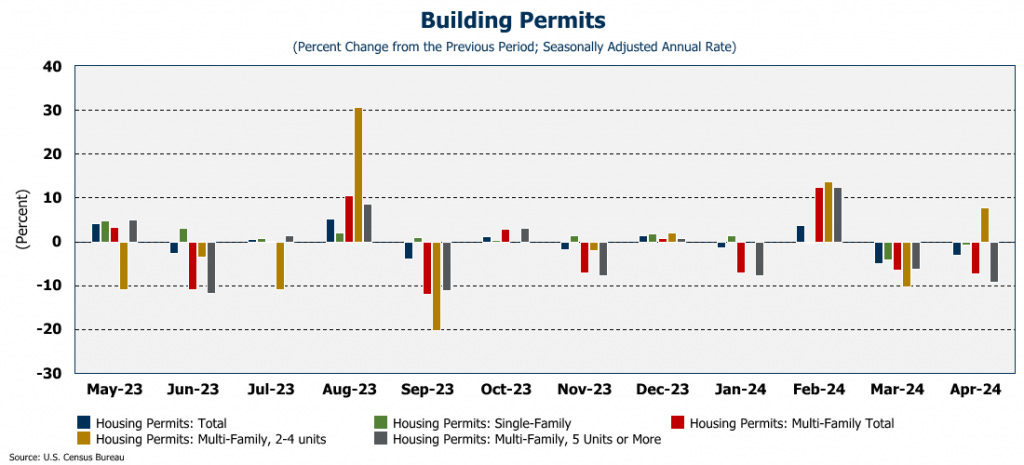

Building Permits

Housing starts, of course, are the result of permits that were issued in months past when home builder confidence wasn’t quite so bad. However, permits are a closer reflection of feelings today. For the second month in a row, building permits are down across the board with single-family permits down 3.0% on an annual basis, and multi-family permits down 7.4%. Only permits for multi-family housing with 2-4 units were up in the month.

In absolute terms, single-family permits dropped to a annual rate of 976K units, the lowest since August 2023. Multi-family permits continue their downward plunge and are now at an annual rate of only 408K units, the lowest since October 2020.

Industrial Production

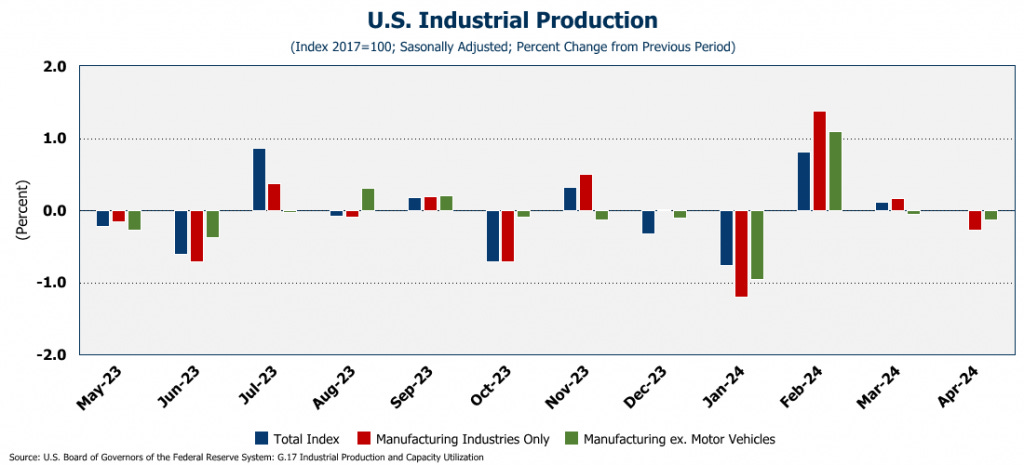

We know from the ISM Manufacturing index that manufacturing in the U.S. has been in recession for more than a year and a half with the ISM Manufacturing Index falling back below 50 in April. This week, we got data on industrial production from the Federal Reserve, and it confirmed the decline. Production for manufacturing industries declined 0.3% for the month, and the previous month was revised significantly lower than initially reported. In fact, 11 of the last 13 months have seen significant downward revisions from the initial reading. (As I have pointed out on several occasions, that has been a broad-based trend across all economic data for the last few years...initially reported numbers revised much lower in the future when no one is really paying attention.) Manufacturing excluding motor vehicles was still down 0.1%. The total industrial production index was flat (0.0%) showing no growth whatsoever between March and April.

Index of Leading Indicators

And, the last bit of data for the week was the Index of Leading Indicators. Previously, I suggested that I might stop reporting on this since they clearly are not doing the very thing they are designed to do. They have now been down for 24 of the last 25 months - more than two years - but there has been no recession. In theory, the index should lead the economy by 6 to 9 months. While GDP is finally slowing, the leading index has completely de-coupled from any measure of the real economy. This is likely due to the fact that excessive government spending (financed by huge fiscal deficits) has artificially kept the economy afloat for two years.

Final Thoughts

I just want to take a moment and thank everyone who has subscribed to this update, and who share it on a regular basis. This update has been going now for 39 weeks. The first of January, I had 88 subscribers. As of today, there are 281 and about twice as many as that are viewing the post each week. If you find it useful, please continue to share it. I want to especially thank those of you who have made a financial pledge to support this effort. I haven't turned that feature on, but I may one day to help cover the cost of the data service I use to compile the numbers and graphs each week.

Also, FOR THIS UPDATE ONLY I am going to turn on comments. You should be able to post comments in the app or on the website. If you have any comments and/or suggestions, please feel free to post them. Due to my own time limitations, I don't usually turn comments on as I simply don't have hours on end to answer questions. But in these 39 weeks, I have only heard from readers that I have met in person and I would appreciate any constructive feedback you have. I want to make this as useful as possible.

Finally, it seems that inflation is everywhere....not just in America. Came across this video this week, and I couldn’t stop laughing. I think we can all understand her frustration.

Until next week.

Thanks for doing this, Alfie. As a new subscriber, I'll look forward to your information. I am not, however, unfamiliar with you, as I knew you/knew of you while you were in Gwinnett County.

Best regards, Tommy Jennings