Weekly Economic Update 05-29-26: Case-Shiller Home Price Index; New Home Sales; Durable Goods; Revised GDP; Personal Income & Spending; and PCE Inflation

First quarter GDP was revised down and the savings rate plunged. The party is coming to an end.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

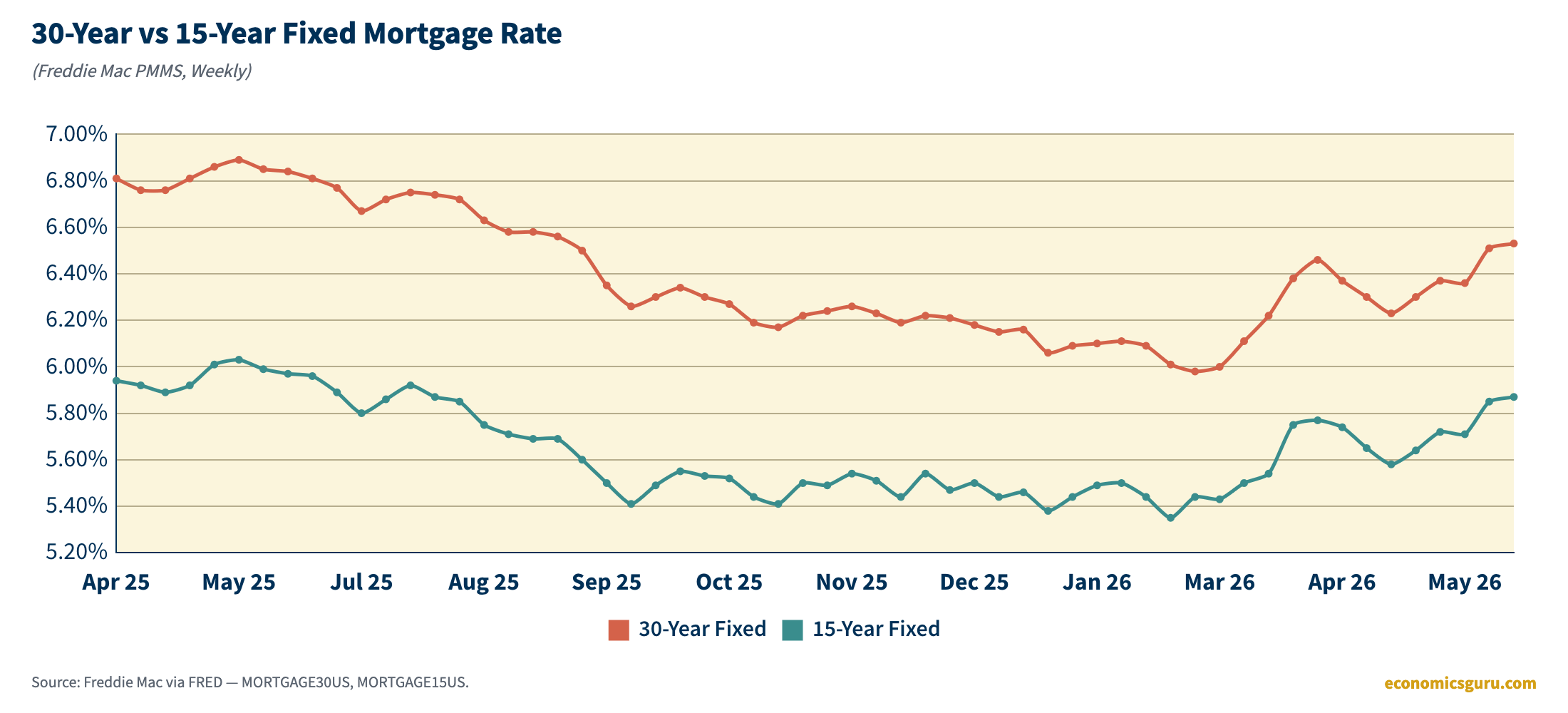

We got a little bit of housing data this week, and if you have been paying attention to the bond market, you know that rates are going up, and with them, mortgage rates are moving up too. The average 30-year fixed conforming rate climbed to 6.65%, up from 6.56% the week before, and is now 30 basis points higher than it was five weeks ago — the highest level since August of last year.

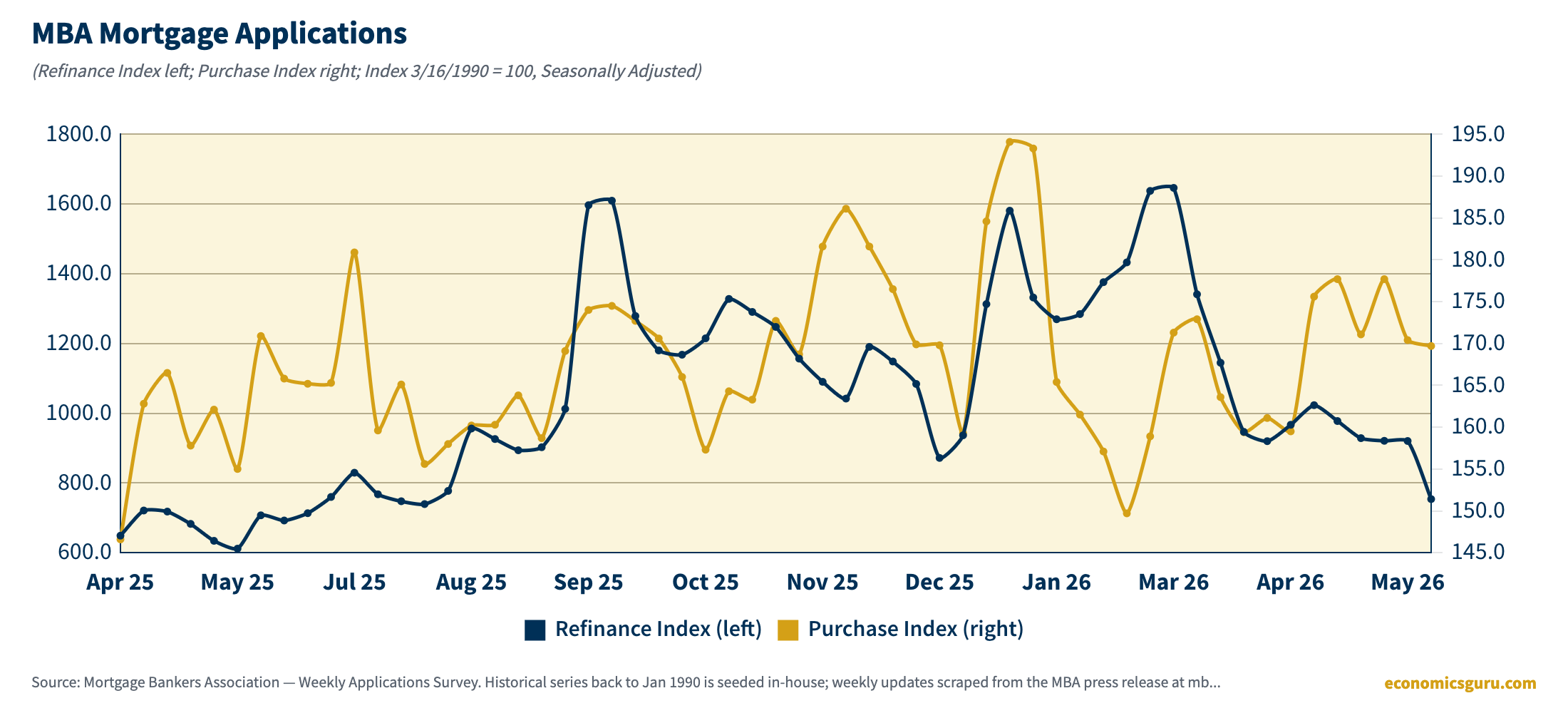

The latest data from the Mortgage Bankers Association told us that mortgage applications fell 8.5% for the week ending May 22 — that is the kind of drop that gets your attention. Almost all of it came from refinancing, where the index dropped 18% in a single week. Purchase applications were essentially flat, down just 0.4%, and still running 5% ahead of a year ago. So this was not buyers walking away; it was refinancers who had been circling lower rates suddenly losing their reason to act.

And as I have been saying, the next rate move by the Fed will be UP. In fact, most bond traders have made an interest rate increase over the next year their base case scenario. The 2-year yield is at or above 4%. The futures market suggests that a quarter-point increase could come in March 2027. I think it will be a lot sooner.

While that will further hurt the housing market, ironically, it may not have that much of an impact on capex spending. As the Chief Economist at Apollo Global Management said in an email this week, “It doesn’t matter what the Fed does. There is FOMO [fear of missing out] among hyperscalers, and AI spending is not sensitive to higher interest rates.”

As you will see below, business investment was the primary driver of first-quarter GDP, not personal consumption. However, corporate profits decelerated sharply in the first quarter: +$40.4B in Q1 vs. +$246.9B in Q4 2025 — a 6-to-1 drop in the quarterly change. The consumer is tapped and getting killed by higher rates. How much longer can AI capex step in and take up the slack? Because once that goes, what’s left?

Keep reading with a 7-day free trial

Subscribe to Alfie Meek's Weekly Economic Digest and Commentary to keep reading this post and get 7 days of free access to the full post archives.