Weekly Economic Update 1-12-24: Consumer Credit; Federal Debt; Consumer Price Index; and Producer Price Index

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Thanks to everyone that is sharing this update! We are adding subscribers nearly every day! If you have comments or suggestions, the best place to add those is on the LinkedIn post that accompanies the update each week. I check those regularly. Also, if you have my e-mail address, direct e-mail works great too!

It is another slow week with respect to the amount of economic data released, but what was released provided some interesting insight into the state of the economy. Let's get to it!

Consumer Credit

Congratulations to all American consumers! They finally made it to $5 TRILLION! That's right! Total consumer credit topped $5 TRILLION in November for the first time ever!

In a period of high inflation, declining real wages, and rapidly depleting savings, how is it that American consumers generated near record nominal spending over the recent Christmas season? Apparently, we borrowed it...and we borrowed A LOT of it.

The expectation was that consumer credit would rise about $9 billion in November. Nope. It jumped about $23.8 billion! In a year when consumer debt exploded, that was the biggest single monthly increase since late 2022. And of that, $19.1 billion was revolving credit! That was the biggest single monthly increase in revolving debt since March 2022, and the second largest monthly jump since we started keeping track! I realize that given inflation and the increase in nominal dollars, records like this are likely to continue, but it still speaks to the extraordinary amount of credit that was extended to consumers in November. In total, Americans now have $1.3 TRILLION of revolving debt, about $1.1 trillion of which is on credit cards.

And those credit cards come with some high interest rates. The average rate for credit card accounts carrying a balance is nearly 23%! That is 700 basis points higher than it was at the beginning of 2022.

Americans have tapped out their savings. The savings rate is hovering at one of the lowest levels in history, and one would think that perhaps that would put a damper on the growth of revolving debt. But apparently not.

On a year-over-year basis, real wages fell for 26 straight months, and have only been positive for 4 of the past 32 months! Again, combined with low savings, one would expect that at some point, the consumer would slow spending. But, revolving debt continues to grow on a year-over-year basis and has done so for 29 straight months, most of which have been double-digit rates.

This simply can not continue. I know I have been saying that for months, but the numbers are starting to get seriously out of balance. Early next month we will get 4th quarter data on delinquent balances and in the next week or so, we should be getting data on personal bankruptcies. Those data will give even more insight into the financial health of the consumer.

How long will the consumer be able to add on to their level of debt? I don't know, but to quote Karl Mordo in Doctor Strange, "the bill comes due. Always."

Federal Debt

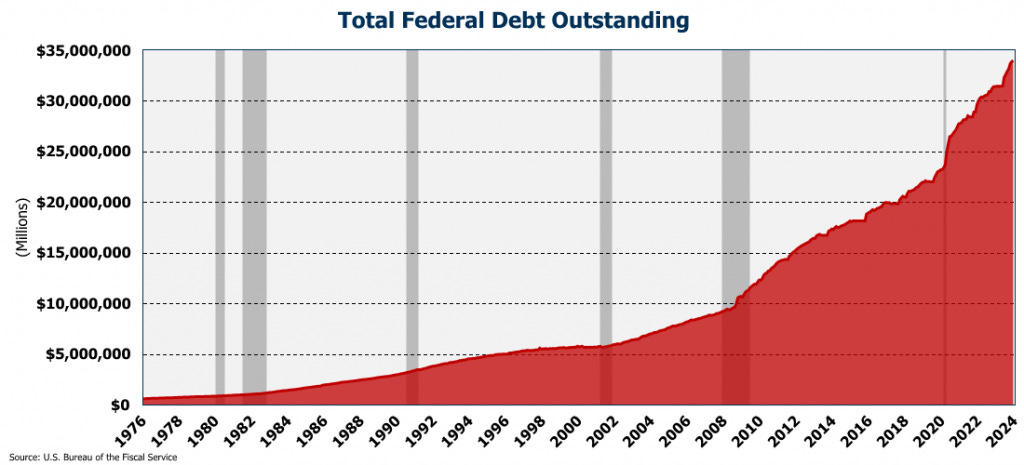

Speaking of the bill coming due....not only did consumer debt hit a major milestone by reaching $5 trillion, but, not to be outdone, the federal government also hit TWO major milestones. The first is that the total federal debt exceeded $34 trillion. We have added $11 trillion to the federal debt since the beginning of COVID - a 46.5% increase. In the third quarter of 2023, nominal GDP was $27.6 trillion. Therefore, our federal debt is now 123% of GDP. On the positive side, we aren't quite as bad off as Venezuela (241%), Sudan (186%), Greece (173%), or Lebanon (151%). However, some of our global competitors like China (77.1%), Mexico (49.6%), South Korea (49.6%), and Australia (22.3%) are in a much better financial position with respect to their debt-to-GDP ratio. Oh, and Russia...they are sitting at only 17.2%.

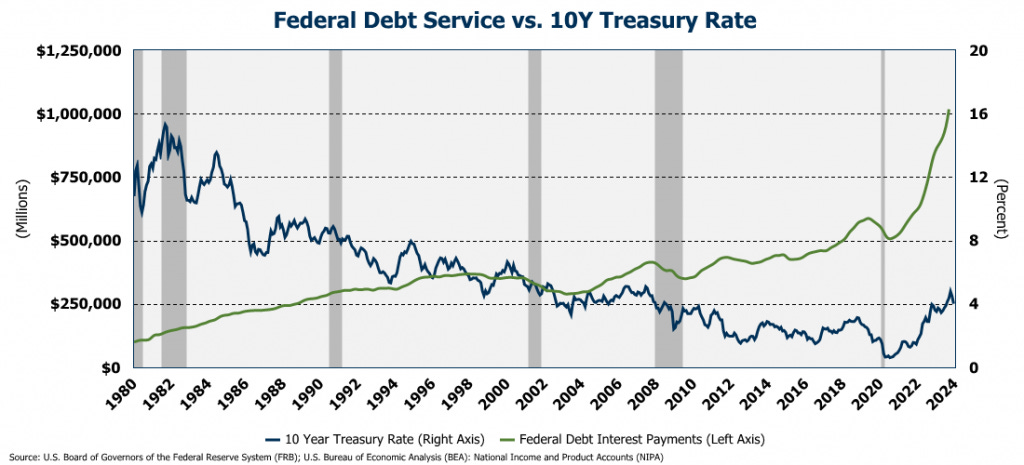

The second major milestone is that the annualized interest payments on that debt just cleared $1 trillion. That is roughly equal to what we spend on national defense. In fact, if you add defense and interest on the debt, you get just over $2 trillion. Over the past 12 months, individual income tax receipts total $2.2 trillion. So, if you are wondering what you are paying for when you start putting together your 2023 taxes, there you go....interest on the debt and guns, bullets, bombs, etc. So how are we paying for everything else? Hmmmmmmmm....

The reason that interest expense has exploded is not only due to all the new debt that has been issued, but also because rates on that debt have risen significantly. As you can see below, since 1980, the rate on the 10-year treasury has slowly trended down, which is the only reason we have been able to fund budget deficits year, after year, after year. But since 2020, not only have we increased the debt 46.5%, but the interest rates required to service that debt have been trending up. In combination, those two factors have driven the exponential growth in federal debt service.

Consumer Price Index

Price inflation as measured by the Consumer Price Index (CPI) ticked up sharply in December to 3.4% from the 3.1% posted in November. The increase was driven in large part by shelter (both rents and owners' equivalent rents) which rose 6.2%, and motor vehicle insurance which was up an astonishing 20.3% year-over-year.

Core-CPI (CPI less food and energy) dropped slightly and came in below 4.0% for the first time since May 2021. While core CPI is moving in the right direction, it is still double the Fed's target of 2%. Making things worse, the Fed's most preferred CPI measure, "super-core" CPI (defined as core CPI services less shelter), ROSE for the third month in a row and is now back ABOVE 4.0%.

In short, the idea that inflation is under control is fantasy, as is the idea of 6-7 rate cuts in 2024, which for some odd reason, is an idea that the market seems to be clinging to. There is no way the Fed cuts rates 6-7 times in 2024 given that inflation is still well above their target, and services inflation is moving in the wrong direction! The comments from New York Federal Reserve President John Williams on Wednesday confirmed as much as he said that "we are still a ways from our price stability goal" and that rates will need to stay high "for some time." A March 2024 rate cut is simply not going to happen. In fact, this inflationary cycle is starting to look a lot like the cycle of the 1970s.....and, from a historical perspective, about 87% of the time, when we experience an inflationary period, we get a "second wave". We may already be seeing the beginnings of such a wave, and if the Fed cuts rates too soon, we will certainly get one.

It is important to remember that we have now completed 3 years of high inflation. So while prices are up only 3.4% from last December, they are up substantially more if you go back to the beginning of this inflationary period. Since January 2020, food is up 20%, housing is up 19%, energy is up 33%, and the previously mentioned auto insurance is up an astonishing 42%! Unfortunately, on a per-employee basis, wages and salaries are up only 11% over the same period. Maybe this is why the American consumers are running up so much debt...our income simply is not keeping up with these price increases.

Producer Price Index

On a month-to-month basis, the headline Producer Price Index (PPI) dropped for the third consecutive month. Year-over-year, the headline PPI is up 1.0%. Core PPI (PPI less food and energy) was up 1.8% and has basically been flat since the summer. However, since January 2021, core PPI is up 16.9%. Services PPI dropped slightly to 1.8%. Intermediate PPI is below zero (disinflationary) but is starting to move higher.

Final Comments

At this time of year, more people than usual are focused on what the economy has for us over the next 12 months. As such, I am giving several economic update presentations to various groups, several of which are private and not open to the public. However, for those that might be interested, I will speaking at the Southwest Gwinnett Chamber's First Friday Breakfast on February 2 where I will be giving an economic update/outlook for 2024. Also, for the third year in a row, I will be giving the keynote address at the Partnership Gwinnett Economic Outlook luncheon, tentatively set for March 21st. Both of these are open to the public. As other engagements are confirmed, I'll make sure to post them here. If you come, please make sure you stop and say "hello."

Until next week.......