Weekly Economic Update 10-25-24: Leading Economic Indicators; Existing Home Sales; New Home Sales; and Durable Goods

Home sales struggle as mortgage rates rise despite the Fed cut

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

I have been out of commission all week on some personal matters, and there wasn’t a lot of data released this week, but I didn’t want to break my streak of 63 consecutive weeks putting out the Weekly Economic Update! (Plus, I now have members so I feel even more obligated!)

The update will be short and sweet this week as there were only a few pieces of economic data released. Plus, at this point, everyone is focused on the election, which, I feel safe in saying, we all just want to be over…especially if you are in the unfortunate position of living in a “swing” state and are bombarded with an incessant stream of political ads, each more extreme and absurd than the last. To quote Mercutio from Shakespeare’s Romeo and Juliet….”a plague on both your houses.”

I once ran for public office. I told my consultant that I didn’t want to do any negative advertising. He paused, looked at me and said, “you know why people run negative ads? Because they work.” Well, then shame on us. But, I guess he was right….I lost. (I was also out-spent 5-to-1. Turns out money works too.)

Leading Economic Indicators

Long-time readers know that have an extra special disdain for the leading economic indicators….primarily because they no longer do what they are supposed to do. Once again, the index fell - this time by 0.5%, which was a bigger drop than expected (full release here). The index has fallen almost every month since early 2022, but the economy has not fallen into recession (at least “officially”) and by most accounts, continues to expand despite the total collapse of the leading index.

As such, we are left to question what possible purpose the index has and why the Conference Board continues to waste time and resources putting it together each month. What does it tell us? It would appear to be telling us nothing about the future state of the economy. I really should just stop including it in this update.

Existing Home Sales

Existing home sales took another tumble this week falling 1% to an annual rate of only 3.84 million units - the lowest level of existing home sales in fourteen years! (Full release here) Like I said above, everyone is just putting on the brakes until we can get this election behind us.

Even with the lower rate of sales, the median sales price rose slightly to $403,825 which is up 3% from a year ago. Despite slower sales, prices just keep rising as inventory is limited. People just don’t want to give up their low mortgage rates because they know that rates that low are unlikely to return in their lifetime. The distance between the average rate on all outstanding mortgage debt and the 30-year rate was narrowing, but was still more than 200 basis points in September. Unfortunately, mortgage rates have only been going UP in October, so that distance is going to widen resulting in even fewer existing homes coming on the market.

One final note on existing homes sales…first-time buyers made up only 26% of purchases, which matched an all-time low. First-time buyers simply can’t get into this housing market. I mentioned above that prices are 3% above last year. But, they are 50% higher than the same period five years ago. And that has put home ownership simply out of reach for new, young, would-be home buyers.

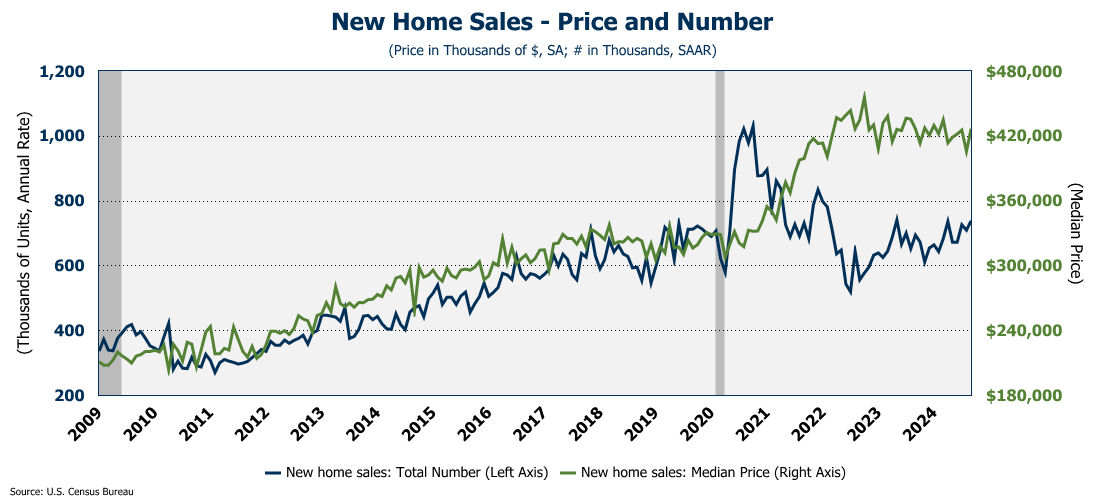

New Home Sales

So, if there are no existing homes, people can just buy new homes, right? Doesn’t always work like that, but it seemed to be the plan in September. When the Fed cut rates and we got a very small pull back in mortgage rates, new home sales jumped to an annual rate of 738K - the highest level since May 2023. That represented an increase of 4.1% month-over-month and they were 6.3% above last year (full release here).

Unfortunately, prices also rose, with the median sales price coming in at $426,600. But even with that increase, prices for new homes are really just moving sideways and bumping around in the $405K to $435K range. That said, mortgage rates moved back up above 7% this week so both existing and new home sales are likely to slow in the coming months.

Durable Goods

For the second month in a row, durable goods orders fell 0.8% (full release here). And, once again, the weakness was in the transportation sector, as orders excluding transportation were up 0.4%. Defense orders also came in strong (they almost always do) rising 6.4% for the month. Orders excluding defense fell 1.1%.

On an annual basis, orders for durable goods are down 2.9% which obviously suggests some weakening in the economy. Further, orders placed for new business equipment also fell, and last month’s data was revised lower, which suggests that firms are being more cautious about making investments.

One More Thing…

I want to send out a HUGE “thank you to my new members this week! Both of these readers had committed to a paid subscription on Substack, but since I am leaving that turned off for now while I build my readership, they instead became members on “Buy Me A Coffee.” Colin Martin became a Bronze member and Dan McRae became my first Silver level member! Thanks so much to both of you!

If you are reading and sharing this update weekly, I invite you to click/scan the QR code below to join Colin and Dan and become a member!

We have some great readers who leave some fantastic comments with their support. But this one from last week is one of my favorites….

Thanks again for all the support!