Weekly Economic Update 2-2-24: Case-Shiller Home Price Index; Consumer Confidence; ISM Manufacturing Index; Job Openings & Quits; Employment Costs; and January Employment

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

There was a good bit of economic data released this week, the most significant of which was the January employment data released earlier today. In addition, the Federal Reserve met this week. You will recall that back in early December, Chair Powell's comments were interpreted as "dovish" and everything has exploded since...the stock market is setting record highs, the dollar is down, gold is up...basically the market is acting like quantitative easing is back in a big way. But, if you actually read his December statement, it really wasn't all that "dovish." The market heard what it wanted to hear. I said several weeks ago that a March rate cut was simply not going to happen, and this week, Chair Powell confirmed it. The Fed voted to keep rates unchanged, and then released a very "hawkish" statement in response to the market's over-reaction from December - quote....“the Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.” As I have showed repeatedly in recent posts, inflation is NOT "moving sustainably toward 2 percent."

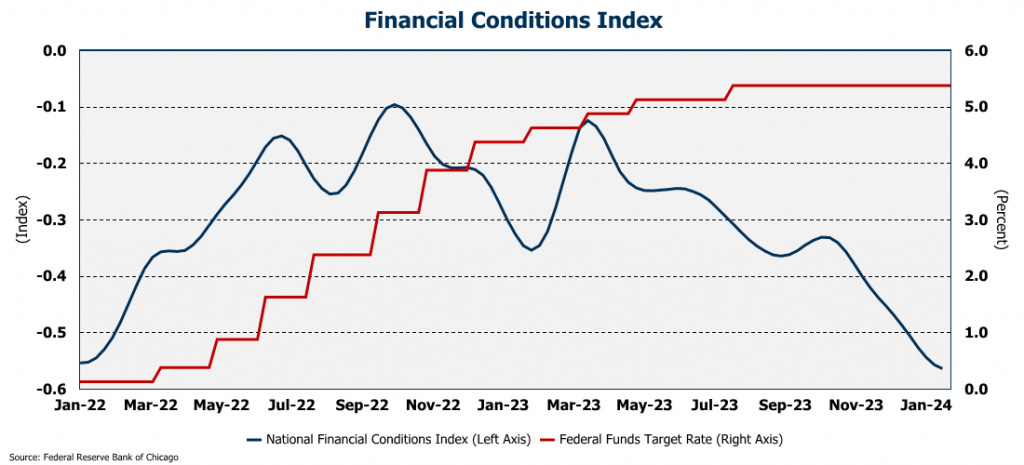

In addition, there were some interesting edits to their statement. First, they removed their comments about "tighter financial conditions," which is understandable given that financial conditions have loosened considerably.

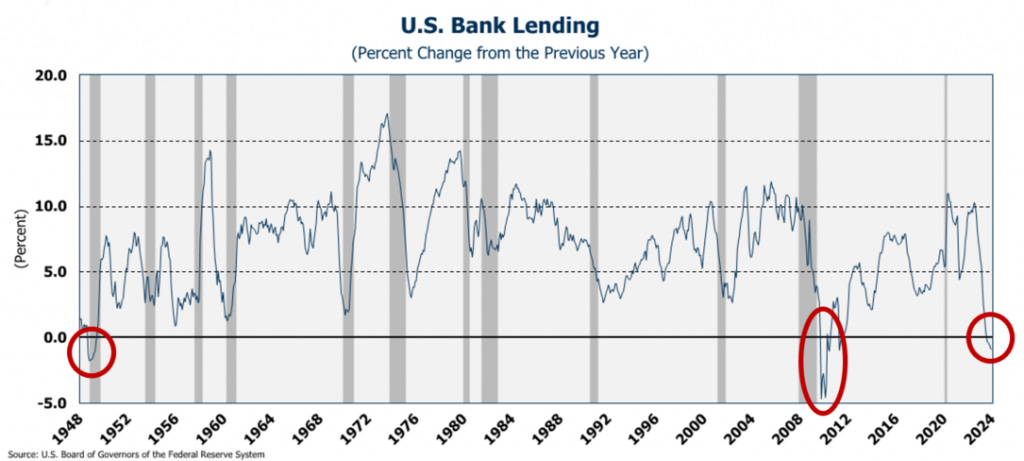

In addition, they also removed the phrase, "the U.S. banking system is sound and resilient." Now THAT should cause some alarm! A quick look at bank lending suggests something is certainly amiss. Currently, bank lending is NEGATIVE on a year over year basis. This has only happened two other times in the last 75 years! Once after the 2008 financial collapse and then back in 1949.

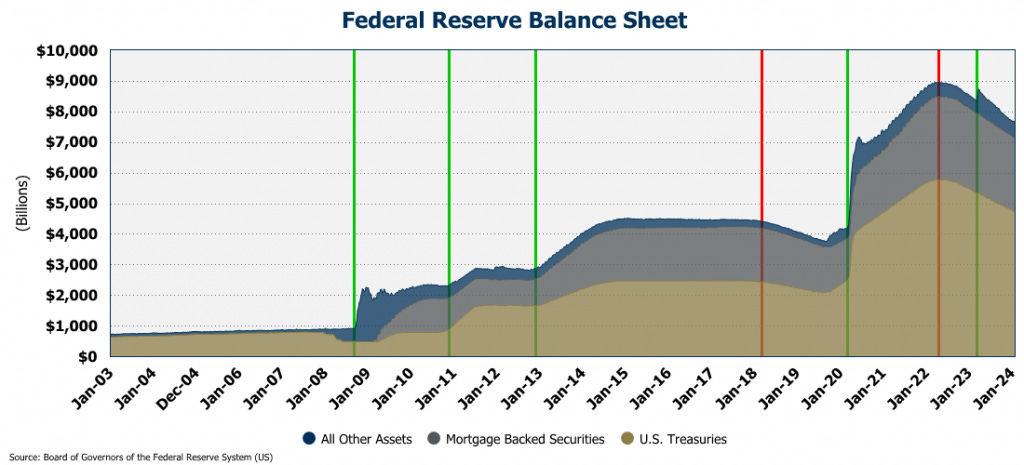

The Fed has been slowly, but consistently, shrinking its balance sheet since April 2022, and has now reduced it by $1.3 trillion. As the Fed continues to shrink its balance sheet, that will put pressure on the banking system (although the balance sheet actually grew slightly last week.)

So, as I have said before, the 6-7 rate cuts the market expected this year simply are not going to happen. When will the first rate cut come? My guess...at the earliest, sometime this summer. But it wouldn't surprise me if it was even later...or even not at all in 2024. "Higher for longer" is what we are in for.

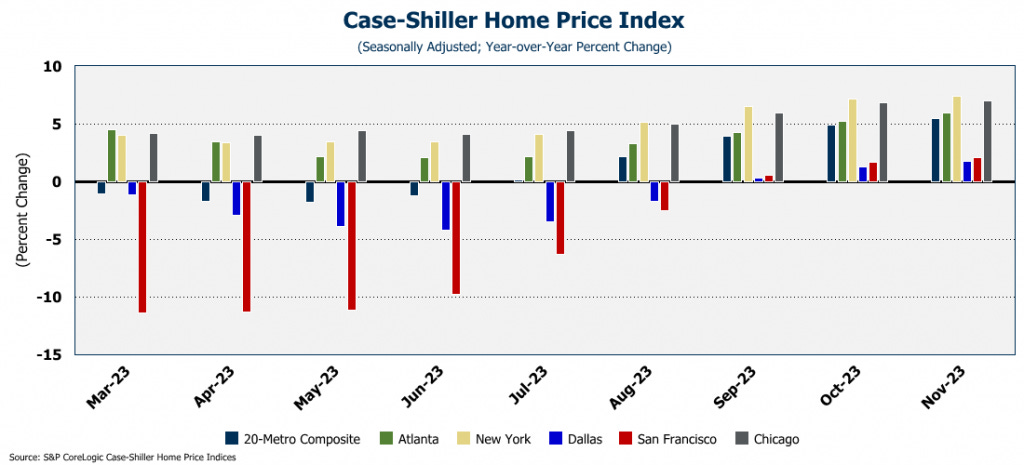

Case-Shiller Home Price Index

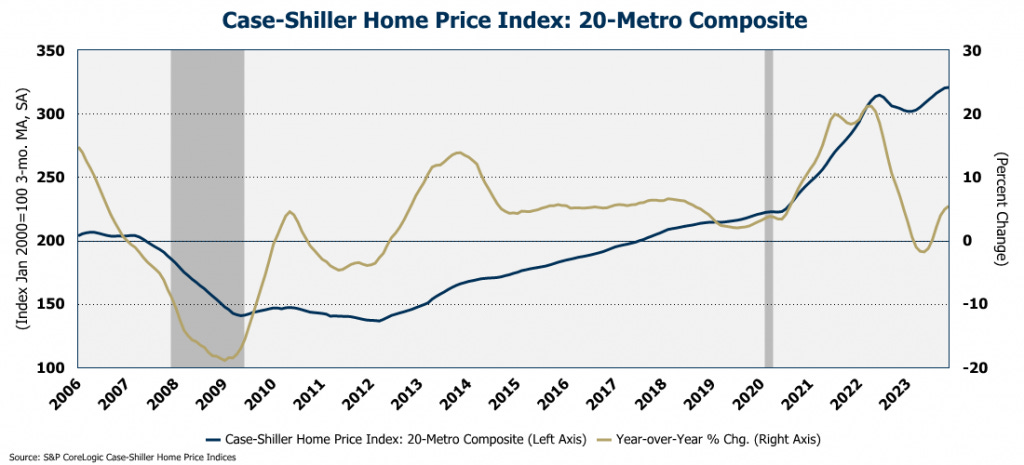

On Tuesday, the Case-Shiller Home Price Index for 20 major metro areas was released. (Note that this data is for November as the index lags considerably.) According to the index, on a year-over-year basis, prices were up 5.4% in November, the biggest increase in a year. Prices have now risen for 10 consecutive months. Even so, it is important to note that this number comes off of very low volume which could be skewing the results. The continuing lack of supply of homes for sale is keeping prices on the rise. And, with the spring home buying season about to begin, home prices will likely continue to rise, at least in the short-term.

As far as the individual metro areas are concerned, only Portland posted a loss. The Atlanta area remains strong posting 6.0% growth, and even San Francisco, where prices had been falling dramatically, posted growth of 2.1%, the third monthly increase in a row.

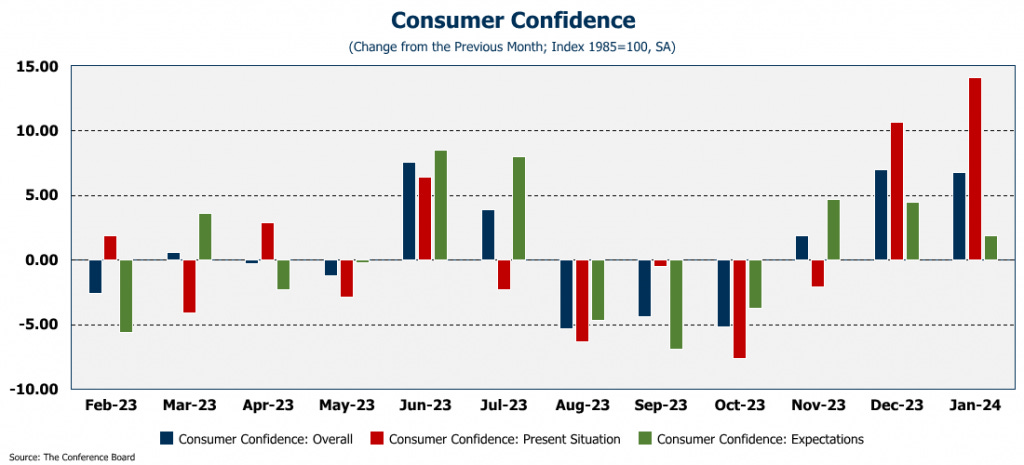

Consumer Confidence

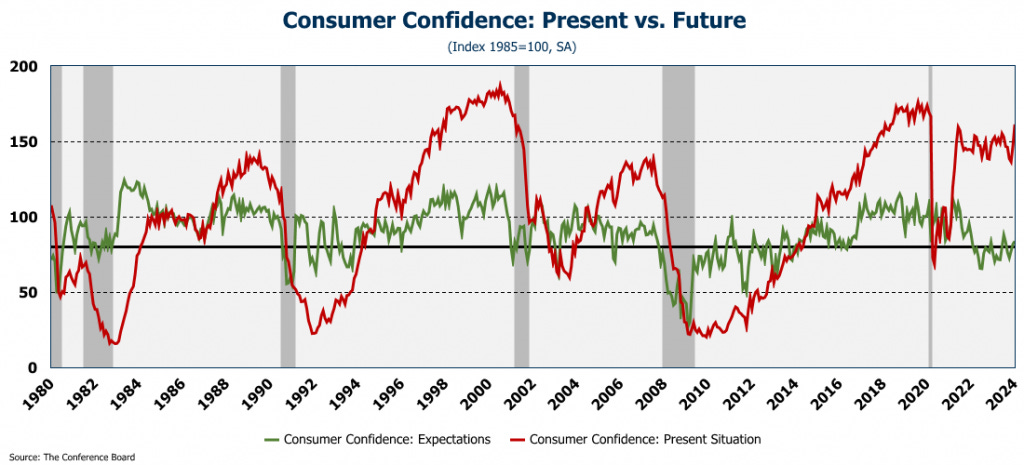

Consumer confidence rose to a three-year high in December, mostly on the strength of the consumer's feelings about their current situation. Surprisingly, despite rising consumer debt, depleted savings, and floundering real wages, consumers seem confident about the economy. These results are similar to what the University of Michigan reported two weeks ago. Even with the improvement in consumer psyche, both the current and future indices are below their pre-COVID peak, although the present situation index is very close to its pre-COVID level.

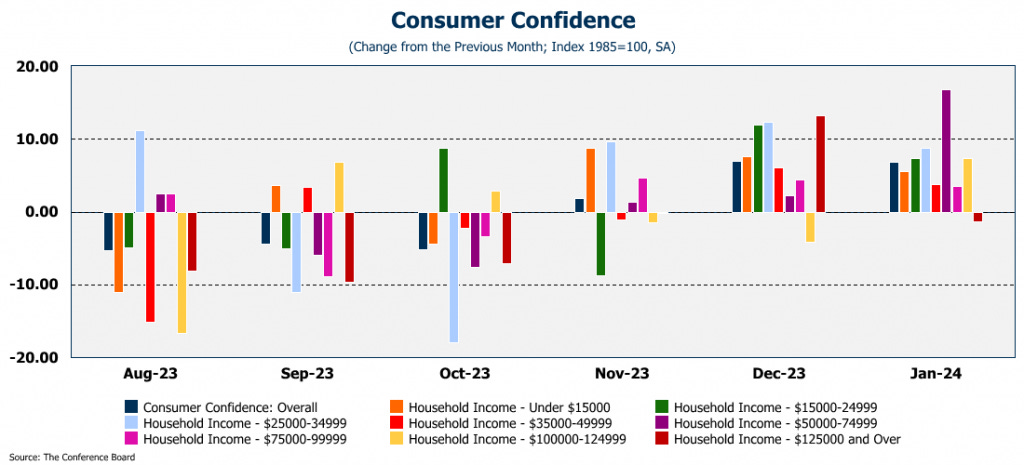

Interestingly, the only income group that posted a decline in consumer confidence are those making $125K or more. The $50K-$75K middle-income group posted the highest increase in confidence after several months of being relatively pessimistic about the economy.

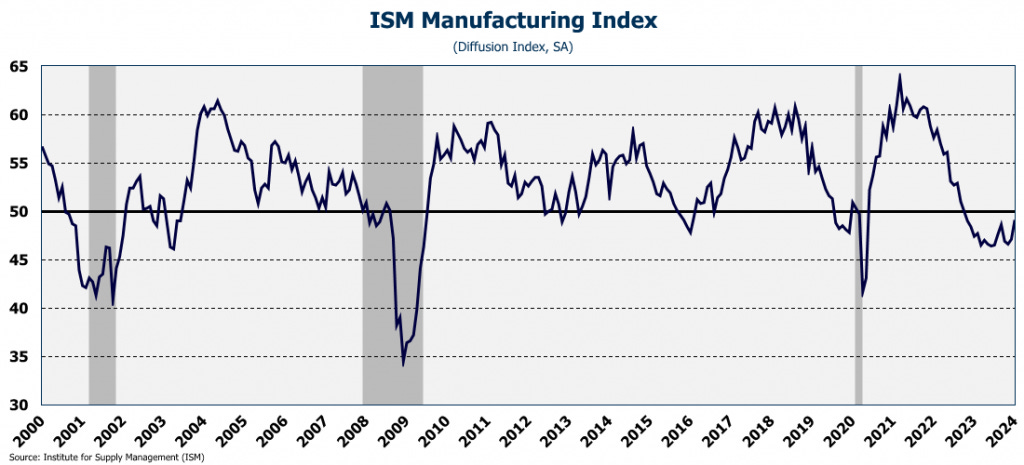

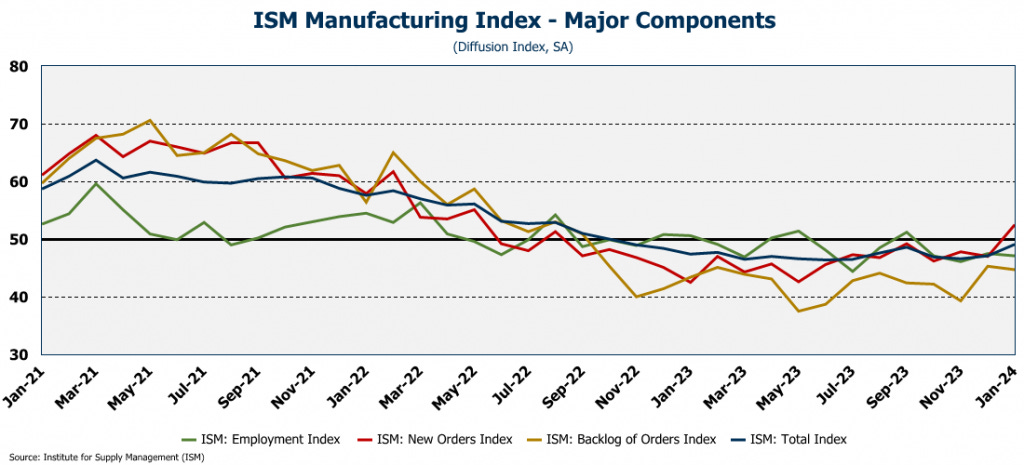

ISM Manufacturing

As measured by the ISM Manufacturing Index, the manufacturing sector in the U.S. declined for the 16th month in a row, although the index did tick up far more than expected (49.1 actual vs 47.2 expectations).

Within the index, employment declined (for the fourth month in a row) , as did the backlog of new orders which has been worsening since late 2022. However, new orders posted the largest monthly advance in more than three years, and provided the one bright spot in an otherwise struggling sector.

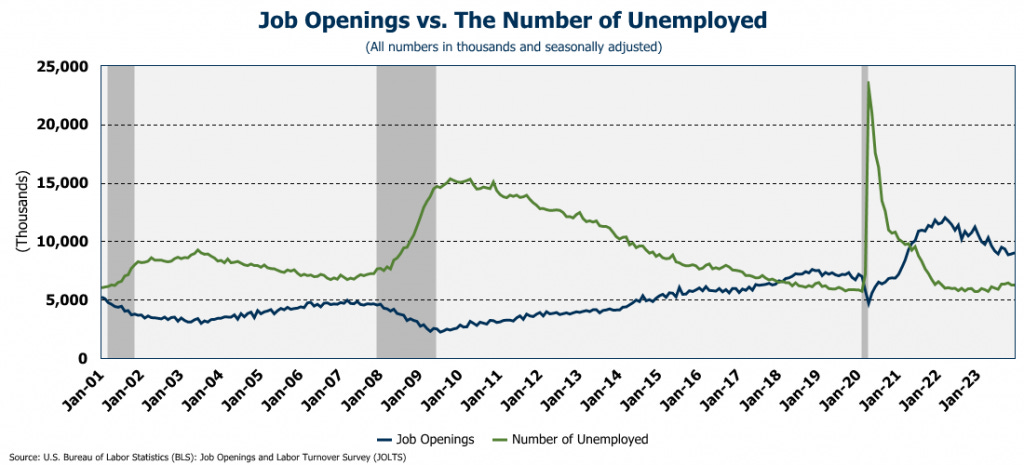

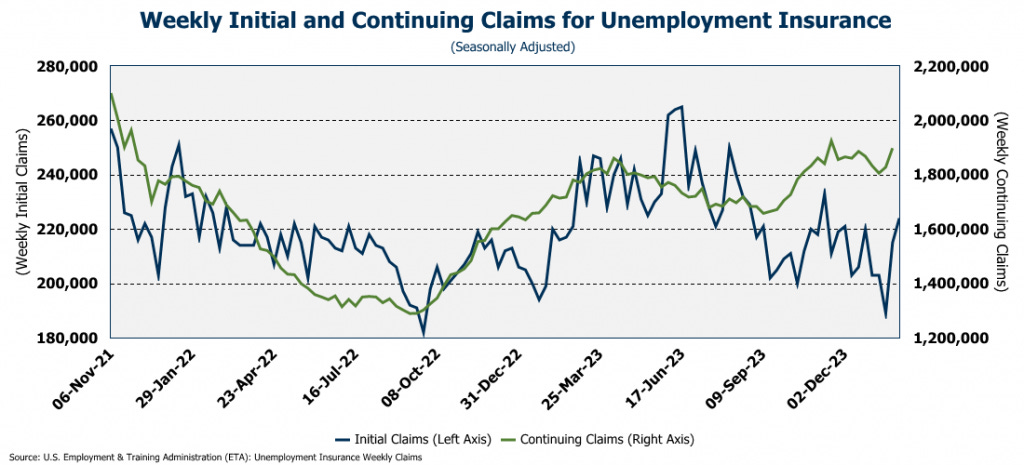

Job Openings, Quits, & Initial Claims

For the last two years job openings have been trending down, suggesting a weakening labor market. In December, job openings surprisingly rose to just over 9 million... the first increase in three months. However, the increase wasn't enough to suggest the trend has turned. We'll watch and see what happens in the coming months.

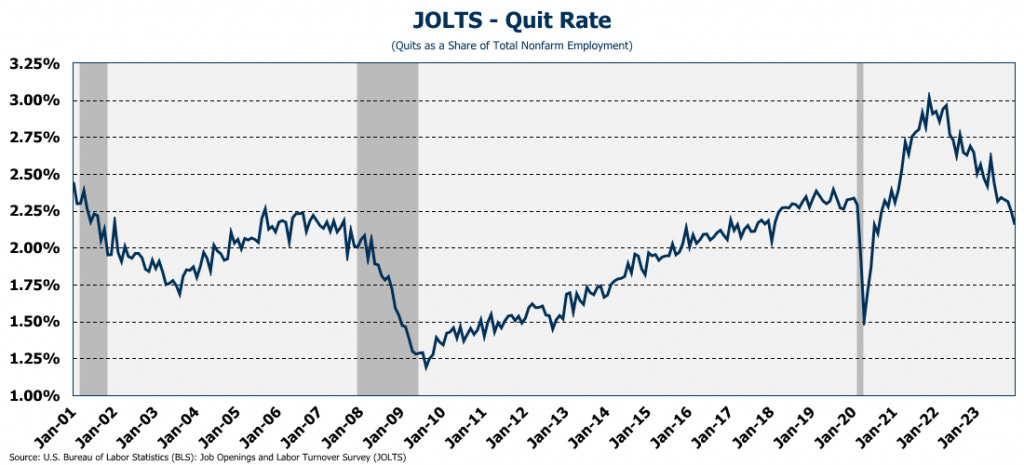

Another indication of the softening labor market is the quit rate, which fell to 2.2% in December with only 3.4 million people walking away from their employer. That is the lowest level in several years - going back before COVID - and far below the post-COVID peak when 4.5 million people quit their job.

To make matters worse, initial claims for unemployment insurance jumped up this week as announced layoffs are starting to take hold. Just this week, UPS announced 12,000 layoffs, but there have been many before that. Over the last three months we have seen layoff announcements including...

Twitch - 35% of workforce

Hasbro - 20% of workforce

Spotify - 17% of workforce

Levi's - 15% of workforce

Zerox - 15% of workforce

Qualtrics - 14% of workforce

Wayfair - 13% of workforce

Duolingo - 10% of workforce

Washington Post - 10% of workforce

eBay - 9% of workforce

Business Insider - 8% of workforce

Charles Schwab - 6% of workforce

Macy's - 4% of workforce

Blackrock - 3% of workforce

Citigroup - 20,000 employees

Pixar - 1,300 employees

Salesforce - 700 employees

American Airlines - 650 employees

The last two weeks represent the biggest two-week jump in claims since 2022 and may be a leading indicator of what is coming in the labor market for the next several months. Continuing claims also rose and we are getting close to 1.9 million which would be the highest since the post-COVID number in December 2021.

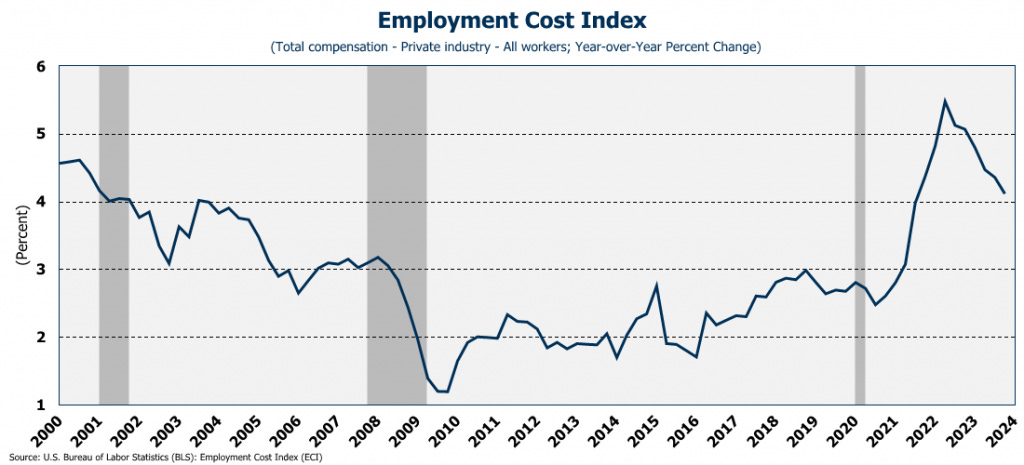

Employment Cost Index

In the fourth quarter of 2023, private sector employment costs were 4.1% higher than Q4 2022. While that was a decrease from the 4.4% in the third quarter, year-over-year employment costs are still growing at a rate not seen since early 2001. Given that labor is a significant input into many goods and nearly all services, recently won wage concessions by the UAW, airline stewards, health care providers, etc. will keep employment costs - and by extension services inflation - elevated. (I would have also included UPS drivers in the list of recently won wage concessions, but the announcement this week of 12,000 layoffs at UPS puts distinctively downward pressure on their employment costs....be careful what you wish for.)

Employment

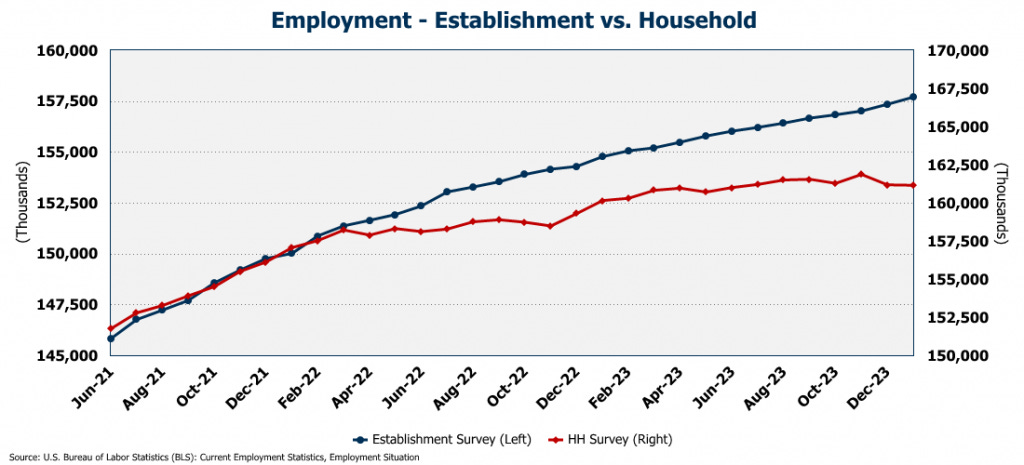

And then, this morning, we got the January jobs report. Apparently, against all odds; against all prognostications of the "experts"; and frankly, against all common sense, we are told that the economy added 355,000 jobs in January! Wow!

Turns out that it actually lost 2.6 million jobs, but once you apply the seasonal adjustment, it grew 355K. Don't get me wrong...adjusting for seasonality is important, but if the adjustment factor was off by only 10%, the number is negative. The 355K number will be touted as representative of a strong labor market, but it isn't.

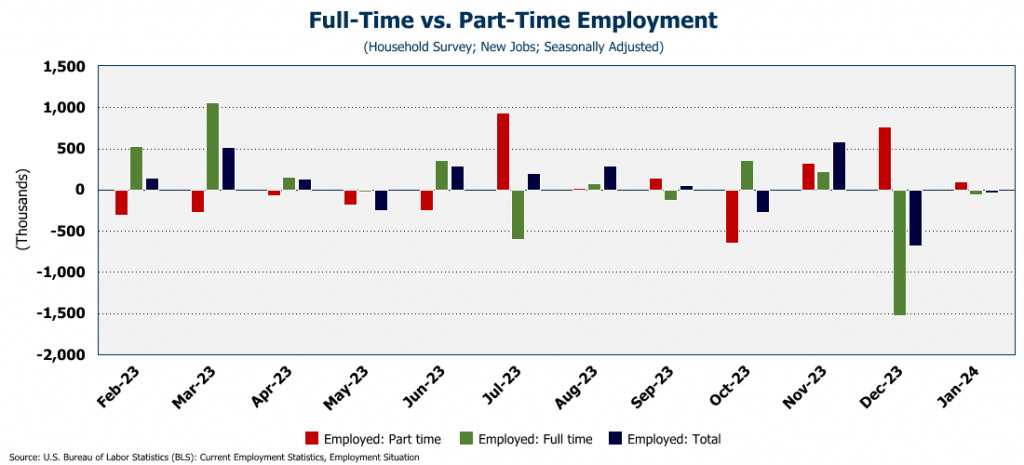

In fact, the establishment number extended its convergence from the payroll number. According to the household survey, the number of people who say they are employed actually dropped 31K. In fact, according to the household data, the labor market was virtually flat and those jobs that were added were all part time, and the number of people reporting to have full-time work dropped for the second month in a row. For the last 12 months, since February 2022, the number of full-time jobs is down 97K while the number of part-time jobs is up 870K. ALL the jobs growth over the past year has been in part-time jobs!

Another interesting piece of news from the release...average hourly earning rose 4.5% over last year, faster than inflation, which means that real earnings rose. This would be great news except that it rose because the number of hours worked fell from 34.3 to 34.1! This may not seem like a big drop, but the last time the work week was so short was when we shut everything down due to COVID.

So, despite the great headline number, as always, the devil is in the details...and the details show that the labor market is weakening.

Final Thoughts...

Finally, this week, I want to thank the Southwest Gwinnett Chamber of Commerce, especially Executive Director Beth Coffey, for having me at their "First Friday Breakfast" this morning! It was a great group and I hope they enjoyed my presentation!