Weekly Economic Update 3-15-24: Comments on the Corporate Income Tax; Consumer Prices; Producer Prices; and Retail Sales

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Listening to the President last Thursday night brought back traumatic memories of being scolded by my aging elementary school principal during my overly mischievous childhood. From an economics perspective, there was much in his speech with which to take issue, as very basic economic concepts seem beyond the man's grasp. I could spend weeks here addressing these, but I will limit myself to only two. First, this week I will focus on the corporate income tax. The President wants to raise the corporate income tax rate, and/or, set some level of minimum tax rate for corporations.

I taught public finance at both the undergraduate and graduate level for a few years at Georgia Tech. Tax policy is obviously a big topic in public finance, and one that always led to great classroom discussions. First, you have to understand two simple facts:

Fact #1: Only people pay taxes

Fact #2: Corporations are not people

Ergo, corporations don't pay taxes. Oh, I know they write the check. We call this "tax impact." But again, see #1 above. When a corporation pays a tax, it is ACTUALLY paid (the "tax incidence") by one of three people groups:

1: Customers - in the form of higher prices

2: Suppliers/employees (i.e., suppliers of labor) - in the form of lower payments/wages

3: Stockholders - in the form of lower returns to capital

When presented with this, students immediately respond "We choose #3! Stick it to the rich people!" But it doesn't work like that. Which of the three groups pays is determined by the various price elasticities of supply and demand of the final products vs. the inputs. Plus, many of those "evil" stockholders are just regular people holding stocks in their 401k's or pension funds.

So, when you raise the corporate tax rate, all you are doing is raising prices, lowering wages, or lowering returns on investments. In other words, you are once again taxing regular people, through yet another avenue. This why lowering the corporate tax rate often leads to lower prices for consumers, higher wages for labor, and higher returns to the stock market. But, since most people don't understand economics, it is easier to pander to people's ignorance than to propose serious policy. But like I said last week, we are governed by unserious people. Yet, the cry "it not fair!" is hard for feckless politicians to ignore.

And speaking of, what exactly is "fair?" I'll address that next Friday.

Consumer Price Index

As was the case last month, CPI again came in hotter than expected across the board. On a year-over-year basis, CPI came in at 3.2%., which is UP from the 3.1% posted in January. That is moving in the WRONG direction. Core CPI (CPI less food and energy) also came in hotter than expected, but was down slightly to 3.8% on an year-over-year basis.

However, services CPI remains very hot. Services constitute a huge portion of the U.S. economy, and services inflation is running 5.2% year-over-year. And while the Fed doesn't necessarily focus on CPI, of all the measures included, probably the most considered by the Fed is "super core" (core services less shelter). That particular measure moved up to 4.5%. It has been moving UP since last September...5 consecutive increases! That is not the direction the Fed needs this to move.

So far, CPI continues to follow the trend of the 1970s, and a second wave is not out of the question. To avoid that situation, the Fed needs to keep rates where they are, or even higher. And they know that. This is why I continue to say that rate cuts are off the table for a while. Even a June rate cuts seems iffy, and if they skip June, they risk looking political if they cut before the election.

Going back to January 2021, food is up 21%; housing is up 20%; energy is up 34%; and auto insurance is up a stunning 45%. All the while, wages and salaries are only up 11.5%. This explains why the savings rate is historically low, and consumer debt is at record highs.

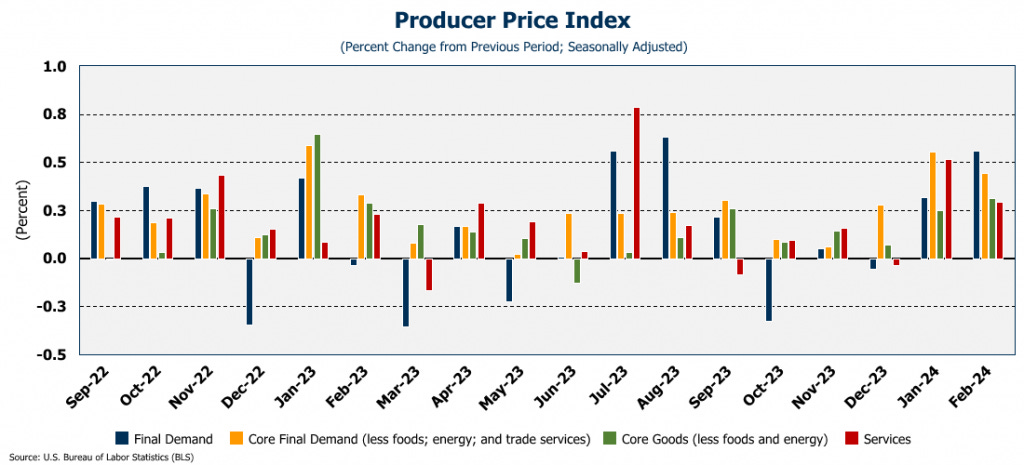

Producer Price Index

And just in case you aren't convinced and still think that inflation is getting under control, the Producer Price Index absolutely exploded in February, rising 0.6% for the month, which is 6.9% on an annualized basis! This is the second month in a row prices at the wholesale level have risen sharply.

Within the index, the PPI for goods rose 1.2% in February (or 15.5% annualized) but about 70% of that is due to the final demand for energy index which rose 4.4% in the month. The final demand for services rose 0.3% (or 3.6% annualized) driven largely by price increases for traveler accommodation services, outpatient care, airline passenger services and alcohol retailing. (Getting ready for the big St. Patrick's Day weekend!)

Price increases at the producer level obviously lead price increases at the consumer level. As mentioned above, CPI is already running hotter than expected, and for the second month in a row, so is PPI. For those looking for the Fed to cut interest rates, this isn't good news. Frankly, the Fed would be totally justified if they RAISED rates! Otherwise, the second inflationary wave shown above is a real possibility.

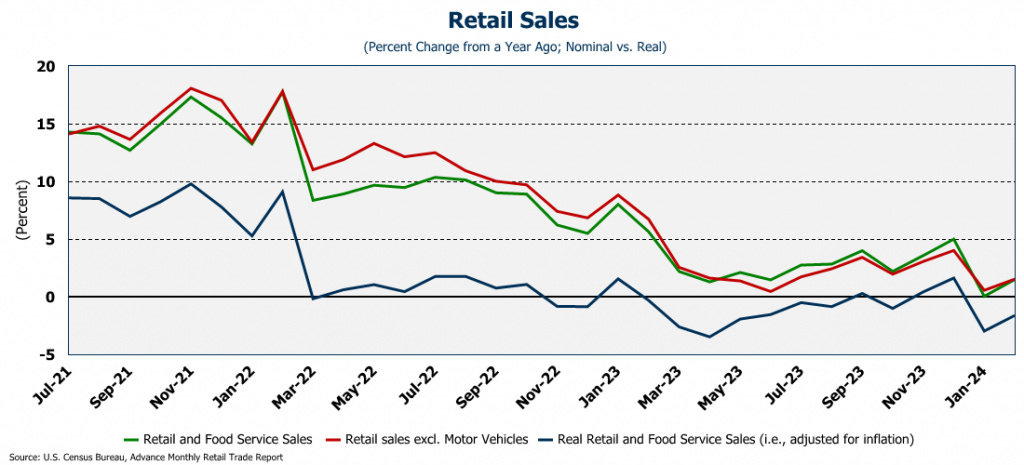

Retail Sales

The reporting of retail sales differs from just about every other economic variable in that the most commonly reported statistic is the nominal number. In other words, it isn't adjusted for inflation. So, when the reporting that retail sales grew 0.6% last month is accompanied by such commentary as "the healthy labor market is adding to incomes and fueling spending" or "faster tax refunds are helping consumers," it totally misses the point. And, when asked about the dismal numbers in the previous month, we hear "the weakness seen in January was likely weather-related." (Of course, the data is "seasonally adjusted" so apparently we are to believe that there has never been bad weather in any previous January.....)

It is all complete silliness. Because, the correct way to measure retail sales would be to adjust for inflation. If inflation is running at 4%, and the retail sales number is up 4% more than it was last year, then consumers didn't really buy any more...they just bought what they did last year. That isn't real growth. (Which is why economists use the word "real" to denote data that has been adjusted for inflation.) So, if we adjust for inflation, February was yet another drop in real retail sales, which have now declined for 12 of the last 16 months! We aren't buying more stuff. We are actually buying less stuff.

But then what about the fact that consumer spending has been such a strong driver of GDP? My favorite comment in the reporting on the retail sales number this week was "consumers have been a reliable growth engine since the middle of last year." While the statement is true, it has nothing to do with retail sales, as they have been negative in real terms. Like I said above, consumers aren't buying more stuff. But they are buying services, which is why that 5-month increase in the "super core" inflation rate discussed above is so concerning. Combine that with the fact that incomes are not keeping up with inflation and the credit cards are starting to get pretty full.

Final Thoughts

Finally, this week, I want to mention one last time that I will be giving the keynote at the Partnership Gwinnett Economic Outlook Luncheon next week on Thursday (March 21st) at the John C. Maxwell Leadership Center in Duluth, GA. Looking forward to seeing everyone there!