Weekly Economic Update 10-11-24: Consumer Credit; Consumer Price Index; and Producer Price Index

The Fed cut rates but inflation is running hotter than expected.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

The disclaimer above was not included in last week’s e-mail. That was an oversight on my part. It is important that I am very clear each week that anything I write in this update represents only my personal opinions and not those of any other group or organization. I will try to be more vigilant in making that clear going forward.

Now on to the data….

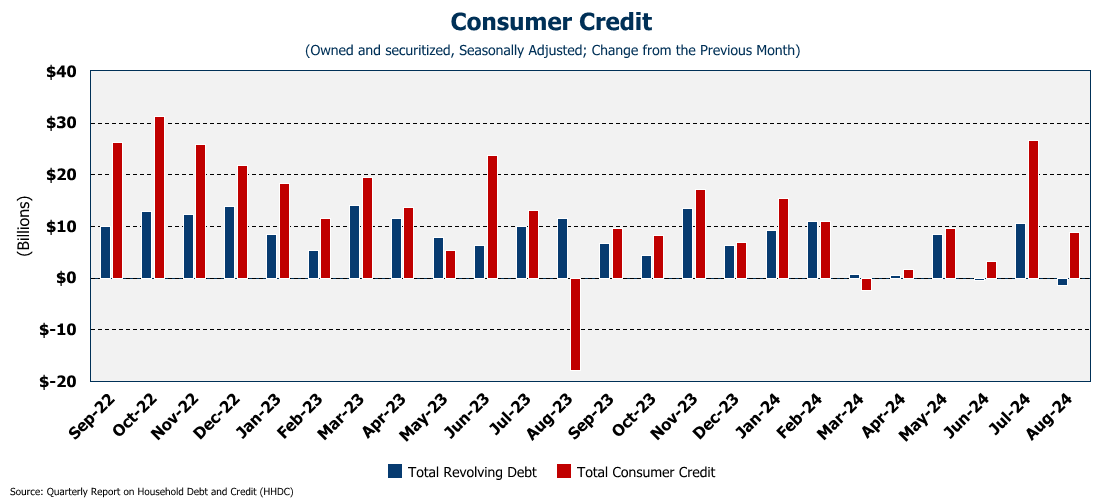

Consumer Credit

There wasn’t a lot of economic data released this week. Monday afternoon we got the latest reading on consumer credit (full release here). Last month I reported that revolving credit (i.e., credit cards) unexpectedly exploded after showing significant slowing in the previous months. Prior to last month, it felt as if the consumer might finally be tapped out, but then in July, they went absolutely crazy and put a additional $10 billion on their cards, and expanded other credit (e.g., auto loans, personal credit, etc.) by an additional $16 billion. Well, now it is looking as if July was a “last hurrah” as the reality of their fiscal situation set in. In August, revolving credit contracted by $1.4 billion.

Total consumer credit now stands at $5.1 TRILLION, with about $1.1 trillion of that on credit cards. And the rate on those cards just hit another all time high at 21.76% (23.37% if you are carrying a balance!)

This data represents August. It will be interesting to see if these rates drop in conjunction with the Fed rate cut in mid-September. They certainly haven’t dropped in the bond market! Consumers were expecting to catch a break when the Fed cut rates…but it hasn’t materialized. With that much debt out there, it isn’t surprising that total personal interest payments are now well above $500 billion annually, and growing…

Who holds all this debt? Turns out, Millennials (those born between 1981 and 1996) are responsible for 42.8% of total outstanding consumer credit. Generation X (those born between 1965 and 1980) is responsible for another third.

Servicing that debt load is killing Millennials’ ability to grow their net worth. They represent less than 10% of total net worth in the country. Even Generation X only holds one-quarter of the net worth. Baby Boomers (those born between 1946-1964) still hold more than half of the total net worth in the United States.

Consumer Price Index (CPI)

The big economic news release this week was the September CPI (full release here). The top-line CPI number continues to drop, falling to 2.4%, but it did come in hotter than the 2.3% that was expected. However, core CPI (CPI less food and energy) was flat, but that was also hotter than expected. The “Super Core” measure (core services less shelter) actually ROSE in the month up to 4.6%. The increase was driven by record high auto insurance, which rose at an astonishing annualized rate of 15.2%.

As I keep pointing out, services inflation is NOT under control. For the most part, this is due to wage pressures. (I refer you to the ILA strike last week.) Because so much of what we purchase are services, this increase in core services inflation is concerning.

In addition to core services, food was up big in September, rising at an annualized rate of 4.9%! On a month-to-month basis, five of the six major food group indices increased. Meats, poultry, fish, and eggs rose 0.8%; fruits and vegetables rose 0.9%; cereals and bakery products rose 0.3%; dairy products rose 0.1%; and “other food at home” rose 0.2%.

With last week’s stronger than expected jobs report, and now inflation coming in hotter than expected across the board, it calls into question the wisdom of the Fed’s 50 basis point rate cut last month. Historically, more than 85% of the time, when we have inflation spike above 6%, there is a second wave that follows. If the Fed continues down this path and cuts rates two more times before the end of the year there is no doubt in my mind that inflation will be higher at the end of 2025 than it is now….regardless of who wins the White House in November.

What makes me even more sure of that forecast is that money supply has once again started to grow. The Fed had been shrinking the money supply since 2022, and that helped bring the rate of inflation down. However, it has once again started to grow, and it is already about $4 trillion above trend. The rate on the 10-year Treasury has gone UP since the Fed cut rates, and is now above 4.1%! As Milton Freidman famously said, “inflation is always and everywhere a monetary phenomenon, in the sense that it is and can be produced ONLY by a more rapid increase in the quantity of money than in output.” M2 grew at an annualized rate of 6.8% in August. That is MUCH faster than output.

Producer Price Index (PPI)

Finally, this morning we got the September reading for the Producer Price Index (PPI). This measures price changes of inputs at the producer level, and can help us see future inflation. Just like CPI, the numbers came in hotter than expected. The top line PPI number came in at 1.8% year-over-year, versus expectations of only 1.6% (full release here). Energy prices helped keep the PPI low, but with tensions rising in the Middle East, that can’t continue. Like with the CPI, food and services prices also moved sharply higher.

However, of more concern is the fact that both core PPI and services PPI are accelerating! Core PPI also came in hotter than expected, rising 2.8% over last year. Expectations were for growth of 2.7%. Service prices continue to accelerate growing at 3.1% annually in September.

I feel safe in saying that another 50 basis point rate cut is off the table for November. In fact, ANY rate cut should be off the table. Inflation is sticky and there is more work to do. Since the Fed cut rates last month, the 10-year treasury is up, as are mortgage rates. They just can’t fool the market anymore. They are printing money, cutting rates, and I suspect we aren’t far from a return to quantitative easing.

New Ways To Support The Weekly Economic Update

As always, I want to thank all the people who share and support this blog. Several of you have pledged a paid subscription. I haven’t turned on that feature, however, because I am still growing the readership. Since only a handful have committed to a “paid” subscription, I am afraid that if I turn it on, it would severely limit my ability to reach new readers. I need as many of you sharing this as possible!

However, a second reason is because each and every week many of you generously contribute to the “buy me a coffee” link and provide encouraging comments. And a lot of you are contributing far more than the “paid” subscription amount! I really appreciate it! This week, thanks go out to Erin Carper and Stephen Hill who bought me a lot of coffee this week!

Over the past few weeks several people have asked how they could do even more to support this effort and keep it going. So, for those of you who regularly “buy a coffee”, I have enabled “memberships” on the “buy me a coffee” site. Now those of you who have pledged a subscription on Substack can fulfill that pledge on “buy me a coffee” by becoming a “member” at the “bronze” level. Those who want to keep this going and contribute beyond that can get a “silver” or “gold” monthly/annual membership and support this effort. You can also get information on a sponsorship of the update, or even a “lifetime” membership!

I am working on ways to provide additional benefits to those higher level subscribers. Stay tuned! But if you enjoy this update and want to keep it going, please click or scan the link below and become a member!

One More Thing…

This week I had the opportunity to speak to the newest Leadership Gwinnett class at their “Economics Day” session. Thanks to Chuck Warbington for the invite. I hope they found the information helpful and insightful. I know a lot of them signed up for this newsletter and are getting their first e-mail today!

We are coming up on the season where I will be doing a lot of economic talks around Georgia and the southeast. I’ll be sharing when and where here in the update and I hope to see of you at those events.