Weekly Economic Update 11-22-24: Industrial Production; Home Builder Confidence; Building Permits; Housing Starts; and the Leading Economic Index

Home builders are more confident...but not pulling new permits quite yet.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Thank you for all the comments via text, LinkedIn, and in-person that I received on last week’s update. You never know which ones are going to be popular and which will be duds. I was thinking last week’s was kind of dud, but I got a LOT of positive response, and more than 1,200 views which is by far the most any single post has ever received!

Also, I had the privilege of speaking the Gwinnett County Chamber Board Retreat this week on the current state of the economy and the challenges facing the new administration. Thank you to Nick Masino, the Chamber President for the invitation and to the board at large. There were some great questions and discussions over lunch. And it was great seeing old friends and colleagues. I enjoyed it and hope they did as well. I am looking forward to being back in Gwinnett on March 27, 2025 where I will present at the annual Partnership Gwinnett Economic Outlook Luncheon!

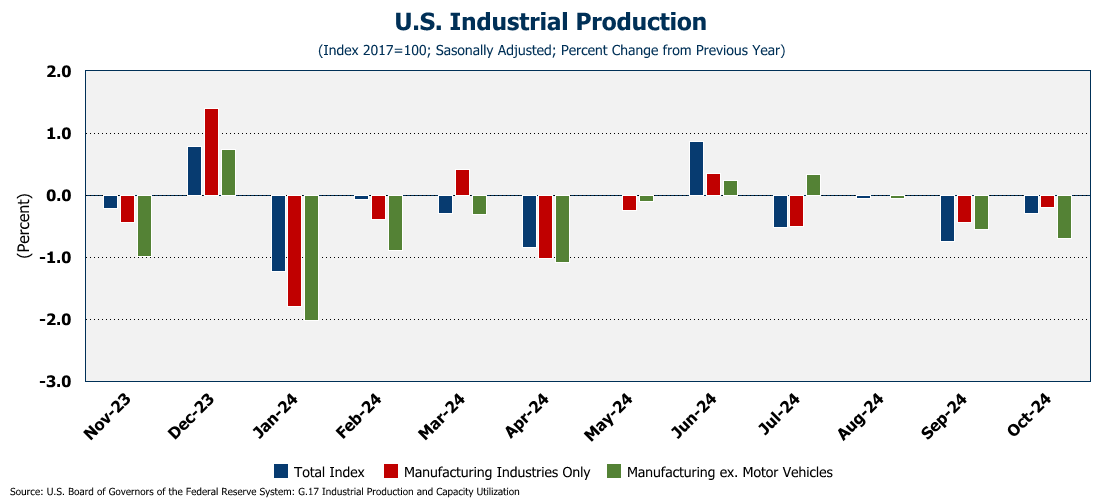

Industrial Production

For the second straight month, industrial production declined in October falling 0.3% year-over-year which was in line with Wall Street’s expectations (full release here). Hurricanes Milton and Helene combined with the Boeing strike to dampen industrial output. But even it you removed those three factors, output would have still be flat on an annual basis from October 2023. And speaking of the previous month…September production was revised down to a drop of 0.5% from the original report of negative 0.3%.

Capacity utilization also fell…again. The capacity utilization rate represents the limits to operating all of the country’s factories, mines, and utilities. As you can see below, utilization has been steadily declining since mid-2022 and now sits at 77.1% total, and 76.1% for manufacturing alone. That is the lowest utilization rate since April 2021 and shows that the industrial portion of the U.S. economy has been gradually slowing for more than 2 years. (See the Leading Economic Index below.)

Home Builder Confidence

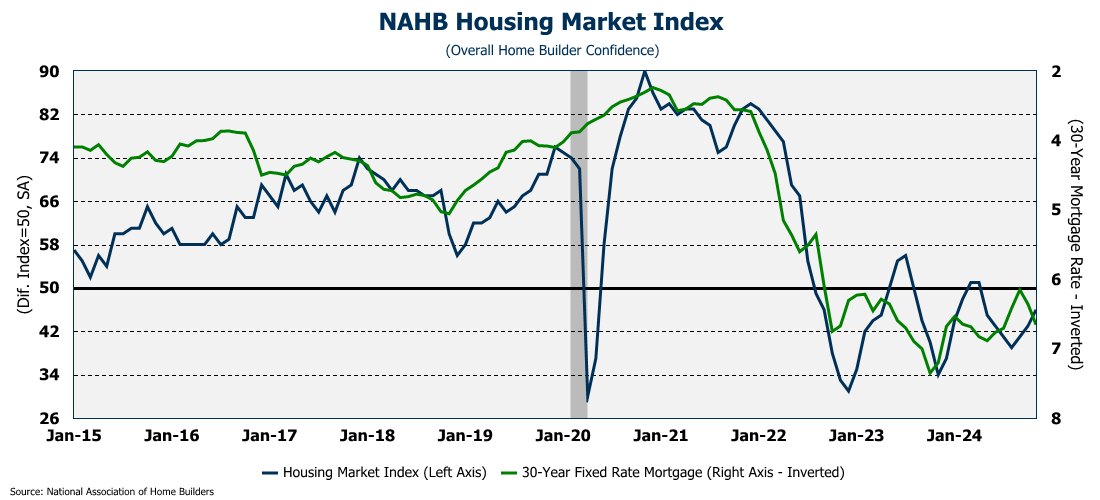

Regardless of how you may personally feel about the recent election, it appears that home builders loved the result. Home builder confidence rose in November and according to the survey, they expect that the new administration will bring regulatory relief which will open the door for significant new construction (full release here). The index rose for the third month in a row to 46, driven mostly by builders’ outlook for the next 6 months. This is the highest level since April and it exceeded expectations. One year ago, the index was at 34.

All three of the index sub-components - outlook for the next 6 months; traffic of prospective buyers; and current single-family sales - moved higher in November. However, the sub-index for the outlook over the next 6 months hit a 2 1/2 year high.

About 31% of builders said they were cutting prices which is about where they have been since July. But the average cut was only 5% which is slightly less than previous months. Further, 60% of builders where using sales incentives, other than prices cuts (like mortgage rate buydowns) to attract buyers. That too is slightly down from the previous month.

Building Permits

Building permits fell 0.6% in October to an annual rate of 1,416,000 units (full release here). Experts were expecting an increase of 0.7%. This was the second consecutive month of a decline in the number of building permits issued. Perhaps the confidence being felt by home builders in November will translate into new building permits next month.

Digging into the data, it was multi-family permits that pulled down the overall number. Single family permits actually rose slightly in October moving up 0.5%. However, multi-family permits were down 3% for the month and that decline was across all types of multi-family units.

Housing Starts

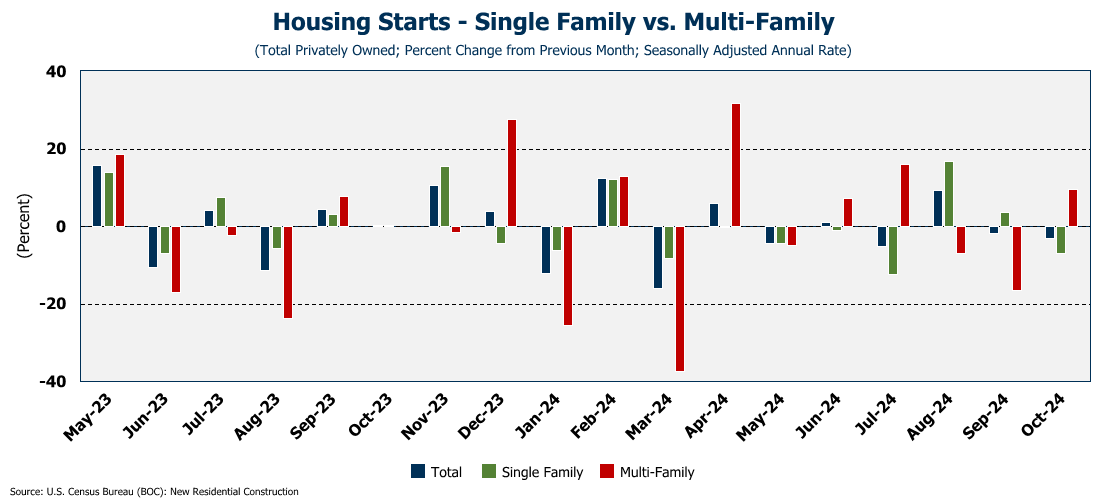

Like permits, housing starts also fell in October 3.1% from September to an annual rate of 1,311,000 units (full release here). Expectations were for a decrease of only 1.5%. Also as was the case with permits, this was the second straight monthly decline. Overall, housing starts are down 4% from last year.

The decline was lead by a sharp drop of 6.9% in single family units. However, multi-family starts rose 9.6% in October. Although feeling more confident, clearly homebuilders are pulling back (at least in the short-term) as mortgage rates are creeping back to 7%.

Existing Home Sales

Existing home sales rose in October, as home-buyers took advantage of “relatively” low mortgage rates which were down about 100 basis points from one year ago (full release here). Sales of previously owned homes rose 3.4% to an annual rate of 3.96 million units. But, the real story is that for the first time since July of 2021, existing home sales posted a year-over-year increase (2.9%).

But even with the year-over-year increase, existing home sales are still below 4 million, which is a key threshold for the housing market. The problem with the housing market is no longer an issue of supply. The months supply of existing homes is back to where it was pre-COVID, and the supply of new homes is well above pre-COVID levels.

The issue isn’t supply…it is affordability. Qualifying income for first-time home buyers is now 100% higher than it was pre-COVID at $100,000! And the first time home buyer index has plummeted. A 100 on that index means that the median income can purchase the median home. The index is now at 65.8 - the lowest it has been since the early 1980s. And what is the “median” home? In October, the “median” home price was $407,200.

Rising prices, coupled with higher mortgage rates are putting first-time home buyers on the sidelines. In October, first-time home buyers made up 27% of purchases…a historically low number. And despite the recent rate cuts by the Fed, mortgages rates are rising once again.

Leading Economic Index

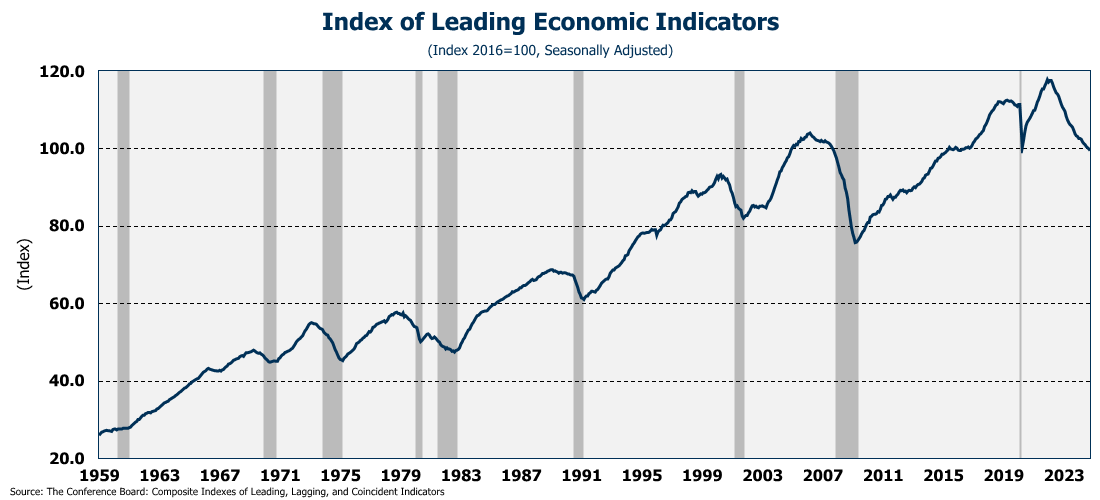

And finally this week…my least favorite economic indicator of all - the Leading Economic Index. Long-time readers know why this index has fallen out of favor with me….it doesn’t seem to do what it is supposed to do! At the top of the release, the Conference Board says “the Leading Economic Index (LEI) provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term.” No it doesn’t! The index has now fallen for 32 consecutive months (full release here). But yet, there has been no “turning point.” There has been no recession, and in fact, all we hear is how strong the economy is!

You may say, “there has been no recession…YET!” And I would agree. But then what constitutes "the near term?” I submit that 32 months is far beyond any reasonable definition of “near term.”

The Leading Index has clearly become uncoupled from GDP, and has even totally disconnected from the Coincident (Current) Economic Index. And if that is the case, what good is it?

One More Thing…

As we prepare for Thanksgiving next week, I want to let all my readers, and especially my supporters, know how thankful I am for their support! Some of you have been with me from the beginning like John Knight in Red Oak Texas, Matt Forshee with Georgia Power, Beth Truelove in White County, Georgia, Carl Snezek, Judy Kerr (the best real estate agent ever!), and Joel Richwine just to name a few. And then, there are those who have signed on as “members” like Andrew Hajduk, Dan McRae, Dave Gmeiner, Chad Teague, Tommy Jennings, Colin Martin, Brad Wood, Carlos Alvarez, and Steve Goins. Their support really helps make this update possible.

If you are reading and sharing this update weekly, I invite you to click/scan the QR code below to join Andrew, Dan, Tommy and the others by becoming a member, or at a minimum, buy a few coffees and support this weekly economic update!

Wishing you all a wonderful Thanksgiving!