Weekly Economic Update 06-13-25: Consumer Credit; Small Business Optimism; Consumer Price Index; and Producer Price Index

Delinquent consumer debt is on the rise, but inflation appears to be improving...for now.

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

Unless you have been living under a rock, you probably know by now that the President of the United States and the world’s richest man had a bit of a kerfuffle last week.

Perhaps you support the President’s policies. Or, maybe you are backing Mr. Musk’s position. Or, more likely, you just enjoyed your popcorn as you watched the show. For a show it was, as the entire episode was, in all likelihood, completely fake. (My working assumption is that most things out of D.C. are fake.). Supporting that position is the fact that they have now “kissed and made up.” I’m sorry…you call someone a pedophile on the largest social media platform in the world…you just don’t come back from that.

However, on the off chance that the rift was genuine, it appears to have roots in Mr. Musk’s desire to cut Federal spending before our country goes completely broke, and the Administration’s complete inability (along with their useless accomplices in Congress) to cut spending in any meaningful way. The current “Big Beautiful Bill” is certainly big, but hardly beautiful. It does virtually nothing to solve the nation’s fiscal woes, and actually makes them markedly worse. The spending cuts are laughable, and while I certainly applaud keeping the current tax rates in place, without any offsetting cuts to spending, even if you accept the rosiest of growth assumptions, the federal government still spends TRILLIONS more than it takes in for as far as the eye can see.

I’ve said it before…we are not governed by serious people, but rather, by feckless politicians who are utterly incompetent at best, and downright malevolent at worst, as they drive our country into financial ruin. Why we continue to put up with it is beyond me. But one thing is certain…elections come every two years, and we get the politicians we deserve. (And before you suggest that, rather than complain, I should run for office myself, you need to know that I have. So yes, I can authoritatively say, we get the politicians we deserve.)

Consumer Credit

If the country is hopelessly in debt, consumers don’t seem to be far behind. In April, consumer credit increased at an annual rate of 4.3%, rising to just over $5.01 trillion (full release here). Revolving credit increased at an annual rate of 7%, and non-revolving credit increased at an annual rate of 3.3%.

Looking at the details, the share of balances that are over 90-day delinquent is rising across all types of debt. Consumers now hold $1.3 trillion of revolving debt, with $1.2 trillion of that on credit cards. Of that $1.2 trillion, 12.3% (or about $145 billion) is more than 90 days past due, and that share is rising sharply.

Now that it has become clear that they have to pay it back, student loan debt, now standing at $1.6 trillion, has a 90+ day delinquency rate of 7.7%, or $123 billion. The percentage of balances that are more than 90 days delinquent are also rising for auto loans as well as mortgages.

Given all this debt, and with interest rates as high as they are, personal interest payments have set an all-time high and now stand at $567 billion per year - more than double what they were at the beginning of 2021.

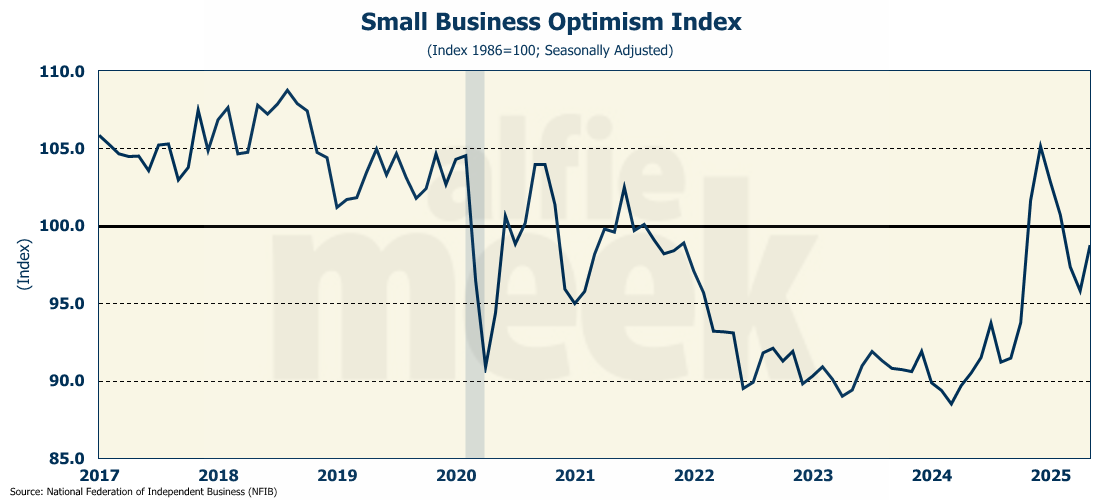

Small Business Optimism Index

Small business optimism rose sharply immediately after the election, which at the time, I pointed out was not a surprise as small businesses are historically optimistic after a Republican wins the White House. However, since then, it has dropped steadily. Until May, when, for the first time this year, it moved up (full release here).

The biggest drivers of the increase in the index were small businesses expecting inflation-adjusted sales to improve (+11) and the economy to improve (+10). The share of firms raising prices was unchanged. These are all good signs and support the idea that the economy should improve from the negative growth posted in the first quarter.

Consumer Price Index

Wednesday, we got the latest data on inflation as measured by the Consumer Price Index (CPI), and what do you know…it once again grew at a slower pace than expected (full release here). On a monthly basis, prices were up by 0.1% in May and 2.4% on an annual basis. That is up from the 2.3% posted in April, but nothing like what the shock-jock media have been telling you was going to happen as a result of the now-infamous tariffs.

Core CPI (CPI less food and energy) fell to 2.7% in May, the lowest it has been since it exploded in April 2021. Finally, super core (core services less shelter) ticked up slightly to 3.1%.

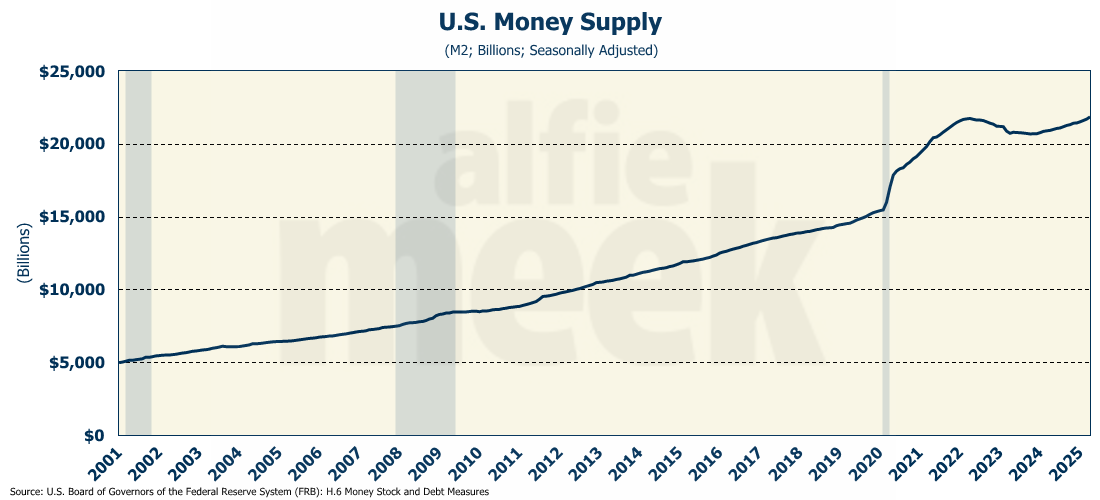

All three measures came in well below “expectations.” The tariff effect just isn’t there. And what inflation we will see in the near term will be a result of excessive money printing, not tariffs. In April, the money supply hit an all-time record, surpassing the previous record set during COVID when the federal government couldn’t give money away fast enough. The annualized monthly growth rate of the money supply in April was 9%. That is inflationary anyway you cut it and will show up over the coming 12-18 months. If the Fed cuts rates, it will only make matters worse.

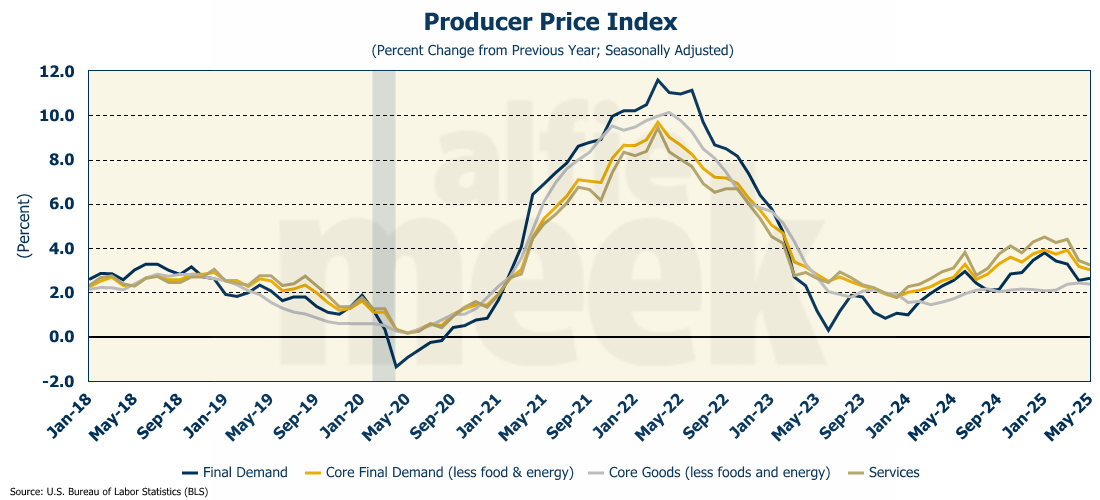

Producer Price Index

The last bit of data we got this week was for prices at the wholesale level. Just like CPI, the Producer Price Index (PPI) rose only 0.1% in May, also less than expected (full release here). Seems those pesky tariffs haven’t even impacted prices at the producer level. The price of lumber fell 2.4% in May; iron and steel were down 7.9%, and even dairy products fell 0.6%.

Again, as seen above, PPI was up for the month of May, but on an annual basis, only PPI final demand was up, rising from 2.5% to 2.6%. The other “top-line” measures of PPI - core final demand, core goods, and services, all fell on a year-over-year basis.

One More Thing…

Happy Father’s Day to all you fathers out there! I will be spending my weekend with my sons, and I can’t wait for some great family time at the lake.

Finally, this week, I want to thank all my “bronze” level members who subscribe for just $8/month. Dave Gmeiner, Colin Martin, Brad Wood, Carlos Alvarez, Steve Goins, Tommy Jennings, Chad Teague, Andrew Imig, Adam Hayes, Kimble Carter, John Mooney, and someone with a “GTwreck” e-mail! Thanks for all your support!

I also have a few supporters who have chosen the monthly option - Rope Roberts and Sarah Jacobs. Thank you all for your monthly support!

Despite all of the wonderful support, it has become quite clear that this little weekly update will not generate enough revenue to pay for the data subscription I use to help with the analysis and create all the graphs. If all of my current subscribers paid just $2.50 per month, it would cover the cost. Of course, in any given week, only about 60% of subscribers are reading the e-mail. But if that 60% contributed about $3.75 per month, the cost would be covered.

As evidenced above, many of you are contributing much more than that, and I do appreciate it. However, if I am unable to cover the cost by the end of this calendar year, I will bring this weekly update to a close in early 2026 when my data subscription is up for renewal. So, if you find this to be worth a few bucks a month, I invite you to join those listed above, and those gold/silver members listed last week, and click/scan the QR code below to support this effort.

If you don’t believe it is worth a few bucks a month, I completely understand. That just tells me that my time is better spent on other endeavors.