Weekly Economic Update 08-23-24: One Year Anniversary; Price Controls; Employment Revisions; Leading Indicators; Consumer Sentiment; Philly Fed Survey; Existing Home Sales; and the National Debt

Sponsored by: LOCI Fiscal Impact Model

The views and opinions expressed in this post are solely those of the author and do not necessarily reflect the views of the Georgia Institute of Technology or the Georgia Board of Regents.

One year ago this week, I published the very first Weekly Economic Digest. When I started, I had envisioned a weekly e-mail/newsletter that honestly reported what was happening in the economy; that would be co-written with a couple of good friends; and would find an interested audience of more than just a few people.

While the friends haven’t been willing to help co-write (although they do provide a lot of topic ideas and critical editing/proofing each week) I think I have hit or exceeded my other goals. I just went back and checked the stats. That first post got a total of 10 views. Week 2 got only 7. Not the best of starts. But it jumped quickly and the week 6 post jumped to 124 views. And it has been growing ever since. In any given week, the posts get about 3x as many views as I have subscribers, so people are reading it, sharing it, and viewing it. Based on so many of the comments I have gotten from readers, I think literally hundreds of you find it useful each week, and I enjoy putting it together far more than I thought I would.

Despite a few vacations, I haven’t missed a single week. I am not promising to keep up that consistent pace (my anniversary is coming up in two weeks and we are going away and I am not promising to get a post out) but I do promise to try to publish the update most weeks. When I turn on the paid subscriptions in October, I hope many of you will find this worth the investment.

Price Controls

This topic made a big splash this week. There isn’t much that all economists can agree on. Very, very little, in fact. But this is one where you will get almost universal agreement. To prove my point, even the political shill, and Nobel-prize winning economist Paul Krugman, who bends over backwards to support most bone-headed economic policies, can’t find the stomach to back this plan. Price controls don’t work. Period. All they do is limit supply, create black markets, result in inefficiencies, and increase prices.

Don’t believe me…read Krugman’s own text book (references are for the 2018 5th edition). According to Krugman, price controls result in “inefficiently low quantity” (p. 133); “inefficient allocation to consumers” (p. 135); “wasted resources” (p. 135); and lead to “the emergence of black markets (p. 136). In short, he points out that “when a governments tries to legislate prices - there are certain predictable and unpleasant side effects” (p. 130). It would be kind of hard for Krugman to come out and support the Harris policies now. But give him time….he’ll figure out a way. In fact, in his latest op-ed, he is trying very hard to have his cake and eat it too. Being partisan before principled can sometimes put you in a bind.

Further, this imagined “price gouging” even IF it was happening is NOT a cause of inflation. I addressed this briefly in what has become my #1-all-time most viewed post, so I wont’ go into a lot of detail here. But as I said then, this just isn't the way the economy works. For corporations to consistently post "above average" profits and drive up prices, you would have to have wide-spread collusion across every major sector of the economy! The same would be true within a particular sector, such as food. Why? Because consumers would start to substitute one good for another. For example, if beef producers colluded to keep beef prices high to gain "above average" profits, consumers would simply move to chicken. The collusion would need to be across not only beef, but all beef substitutes. And, of course, there would be a huge incentive for a particular company to lower their prices and gain market share! That incentive would drive companies to cheat, which would collapse the collusion and profits (and prices) would settle back to a market equilibrium. Again, “corporate greed” is simply not a driver of the sustained inflation we have experienced since 2021. And the “medicine” proposed last week by candidate Harris, would only serve to kill the patient.

Employment Revisions

Another topic that made a splash this week was the revisions to the employment numbers between March 2023 and March 2024. Consistent readers of this update will know that nearly every month the establishment payroll numbers are revised lower, AND that the establishment numbers have been diverging from the household survey quite significantly. Well, on Wednesday, the BLS did their annual “benchmark revision” and admitted that overall employment for those 12 months was over-stated by 818K jobs!! That means that instead of the monthly average of 242K during those 12 months, the actual average was closer to 173K. I know we are all shocked to learn that job growth was less than we were told - but nearly a third! I will have more on this when my data service gets around to updating their database I can see the revised data graphically. But for now, it appears the revision was largely in high paying sectors, including professional services (revised down 358K or 1.6%); manufacturing (revised down 115K or 0.9%) as well as the leisure and hospitality sector (revised down 150K or 0.9%). And these “official” revisions through March call into serious question the employment data released since then! All told, I would guess that the employment numbers are over-stated by more than 1M. We’ll see what we get in early September.

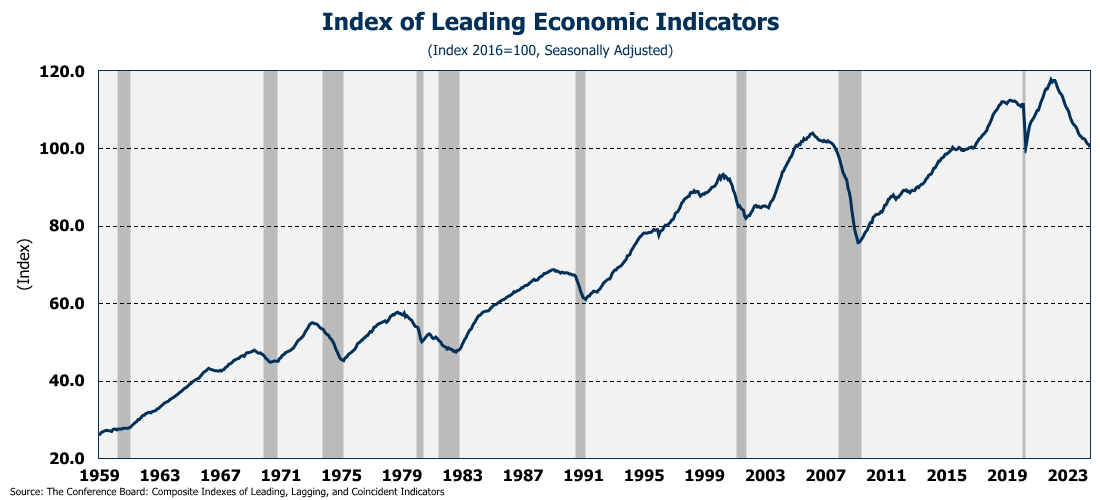

Leading Economic Indicators

The Index of Leading Economic Indicators were down for the 31st month in a row. 31 months. For more than two and a half years, this index of economic indicators has fallen, and is now where it was at the depths of the COVID lockdown. Think about that. These indicators are where they were when we shut down the entire economy (full release here).

And yet, we are told nearly every day, that the economy is doing great! With the exception of the financial crisis in 2007-09, this is the longest and deepest decline in in the leading index since the mid 1970’s. But fear not! Senior analysts at the Conference Board assure us that “the six-month annual growth rate no longer signals recession ahead.” Well, that’s comforting. Was it signaling one before? Because the way they said that, makes me think it was. And if so, where is the recession? I am confused.

But it gets better! While the index apparently does not “signal a recession ahead,” here is how they described the most recent reading….”weakness was widespread among non-financial components. A sharp deterioration in new orders, persistently weak consumer expectations of business conditions, and softer building permits and hours worked in manufacturing drove the decline, together with the still-negative yield spread." Wow. But again, no recession ahead! I think they are right. There is no recession ahead…because we are in one now!

Consumer Sentiment

Well, it doesn’t matter what the Leading Index says because, according the University of Michigan, consumer sentiment rose, and actually came in a little higher than expected at 67.8! The increase was driven entirely by the future expectations index which rose 3.3 points, the largest monthly increase since January (full release here). However, consumer’s feelings about the present continued on a downward trend falling for the fifth consecutive month. Ever optimistic, while things seem bad now, consumers expect the future to be better. Let’s hope they are right.

Philadelphia Fed Business Outlook Survey

Consumer sentiment may have moved up in August, but businesses certainly aren’t more optimistic. The Philadelphia Fed Business Outlook Survey index (full release here) crashed -25.1 in August, the lowest level since COVID. (That seems to be a theme this week.)

Digging into the survey, we see that employment, capital expenditures, and new orders were are all down in August. But most interesting are the prices indices. If we look at the prices received less prices paid indices, we see that margins continue to be compressed, and have been for the last three years! Don’t talk to me about price gouging! “Greedy” businesses are not stealing your hard earned money - the government is - through taxes and inflation. They only blame business to deflect and keep you from seeing what is really happening.

Existing Home Sales

On Thursday, we got a small surprise when existing home sales actually rose for the first time in 5 months by 1.3% to 3.95 million annual units (full release here). Even so, existing home sales are still running down 2.5% on a year-over-year basis. They haven’t posted a year-over-year increase since mid-2021. It is hard to get real excited about this small uptick when this is the lowest level of home sales for the month of July since 2010.

On a seasonally-adjusted basis, the price of an existing home hit an all-time high at $407K. Even with the rising prices, most homes were on the market for less than a month, with the average length coming in at 24 days. And a quarter of those homes sold for more than the asking price. Clearly there continues to be limited supply in the market. Given that Fed rate cut is all but assured in September, we can expect an increase in demand…but I don’t think there will be much an impact on supply. Therefore, prices are only headed higher.

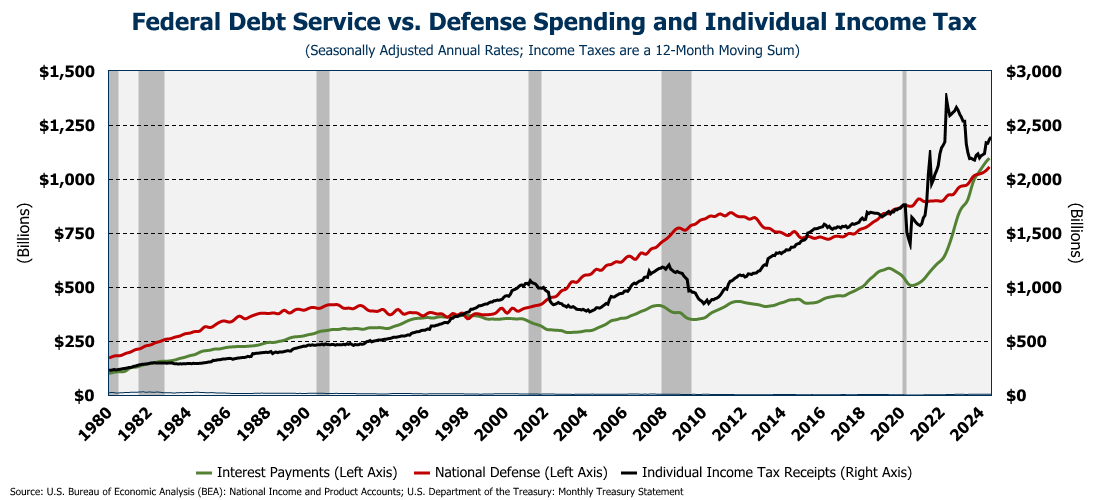

National Debt

The most recent numbers on the federal debt have been released and we crossed the $35 TRILLION mark. With 10-year bond rates averaging about 4.25%, that is a lot of interest! In fact, it is about $1.1 TRILLION in interest per year.

That is a lot of interest. In fact, we are now spending well more on interest than we are on our national defense. And roughly half of all individual income tax receipts go to pay interest on the federal debt.

I am reminded of something Milton Friedman once said….“Keep your eye on how much the government is spending, because that is the true tax. There is no such thing as an unbalanced budget. You PAY FOR IT either in the form of taxes, or indirectly in the form of inflation or debt.”

We are currently paying for it in all three ways. And of the three, inflation is the most regressive and insidious tax of them all.

Final Thoughts

Last week I forgot to add the hyperlink to the “buy me a coffee” graphic. The picture was there…but the link was not. Thanks to all those who sent me a message telling me the link was broken, and a special “thank you” to Chris Braun and Colin Martin who figured it out and got there anyway and bought me some coffee! It is fixed this week and hopefully I won’t make that mistake again. If you would like to help support this work, please click image below.

Or, even better, go ahead and commit to an $8 monthly subscription once I turn them on in October. Knowing in advance how many people are willing to support this effort will help me plan as I move forward.

The Weekly Economic Update is sponsored by: